– War on Taxes: 1964 to 2011

– By: Larry Walker, Jr. –

“The largest single barrier to full employment of our manpower and resources and to a higher rate of economic growth is the unrealistically heavy drag of federal income taxes on private purchasing power, initiative and incentive.” ~John F. Kennedy, Jan. 24, 1963, special message to Congress on tax reduction and reform

Recap: 1776 to 1912

In 1765, Great Britain imposed a series of taxes upon the American Colonies, in order to pay for its lengthy French and Indian War (1754-1763). After the war, the British forced upon the Colonies, the Stamp Act of 1765, requiring the purchase of tax stamps for any printed documents including newspapers, legal documents, marriage licenses and more. This was followed by the Townshend Acts of 1767 which were passed: to raise revenue in order to pay the salaries of governors and judges so that they would be independent of colonial rule; to create a more effective means of enforcing compliance with trade regulations; to punish the province of New York for failing to comply with the 1765 Quartering Act; and to establish as precedent the British Parliament’s right to tax.

Just like the Tea Party Movement of today, our founding fathers resented insidious taxes and regulations imposed upon them without their consent. Then as now, it is simply a matter of ‘taxation without representation’, an act which early Americans likened to tyranny. By 1773, when the East India Company was granted a virtual monopoly on the importation of tea, it was the last straw. In protest, a group of Boston citizens disguised as Mohawk Indians boarded a ship and dumped 342 chests of tea into Boston harbor. The Revolutionary War ensued, and the United States of America was born. Today, the Affordable Care Act is only a symptom of the disease. The disease being: overregulation, overburdensome covert and overt taxes, unsustainable federal debt, and a small minority of ideologues, with socialist tendencies, forcing their will upon the people.

The first income tax proposed by the United States Government was intended to fund the American Civil War (1861). Prior to this, the government was funded strictly through customs duties, tariffs levied on imported goods. During the War of 1812, the government experimented briefly with excise taxes on certain goods, commodities, housing, slaves and land, but a tax on income was out of the question. What is significant is that prior to 1861, or for the first 86 years of American history, whether a citizen had an annual income of $800, $250,000, $1,000,000 or $10,000,000, every dime was considered to be private property of the individual, and not subject to any federal claim.

In 1862, the first Revenue Act was revised, before any tax was due, and the Revenue Act of 1862 launched the first progressive rate tax in U.S. history. The Act established the office of the Commissioner of Internal Revenue, and specified that the Federal income tax was a temporary measure that would terminate in the year 1866. Annual income of U.S. residents, to the extent it exceeded $600 ($13,400 in 2011 dollars), was taxed at a rate of 3.0%; those earning over $10,000 per year ($224,000 in 2011 dollars) were taxed at a 5.0% rate. Through 1912, the income tax only existed for 11 out of the first 137 years of American history, from 1862 to 1872, while no income tax was imposed upon private citizens for 126 years. The income tax was a temporary measure imposed to fund the American Civil War. During the era, the highest tax rate assessed on married couples occurred between 1865 and 1866, when those earning the equivalent of $250,000 (in 2011 dollars) paid a tax of 8.4%, those earning $1,000,000 paid 9.6%, and those earning $10,000,000 incurred a tax rate of just 10.0%.

In the midst of the Panic of 1893, an amendment to the Wilson-Gorman Tariff Act of 1894 was passed, establishing a flat 2.0% tax on all incomes above $4,000 per year (about $104,000 today). The amendment would have exempted from taxation the salaries of state and local officials, federal judges, and the president. Believing the tax to be unconstitutional, President Grover Cleveland refused to sign it. The Act became law in 1894 without his signature, but was ruled unconstitutional by the U.S. Supreme Court in the following year.

Thus America remained the land of the free, free of an income tax from 1873 through 1912. But behind the scenes, the Democrat Party was fast at work, conjuring legislation which would ultimately destroy the freedoms won by Americans in 1776. Democrats proposed a constitutional income tax amendment in their party platforms of 1896 and 1908. Theodore Roosevelt endorsed both an income tax and an inheritance tax, and in 1908, became the first President of the United States to openly propose that the political power of government be used to redistribute wealth.

In 1909, the income tax amendment passed overwhelmingly in the Congress and was sent off to the states. The last state ratified the amendment on February 13, 1913. The Sixteenth Amendment owes its existence mainly to the West and South, where individual incomes of $5,000 or more were comparatively few. Sold to the public as a tax on the rich, the income tax initially applied to less than 1.0% of the population, but that would be short lived. The aspirations of power hungry, greedy and wasteful politicians would soon change the federal government into the conundrum it is today.

Recap: 1913 to 1963

In April of 1913, President Woodrow Wilson summoned a special session of Congress to confront the perennial tariff question. He was the first president since John Adams to make an appeal directly to Congress. Under the guise of reducing tariffs, the Act turned out to be nothing more than a means of reinstituting a federal income tax. The argument followed that since a reduction in tariff duties would lead to lost revenue, an income tax would be required to makeup the shortfall. We should be mindful of this deception as Barack Obama attempts to twist arms during his upcoming special session.

World War I commenced on July 28, 1914 and lasted until November 11, 1918. Since the income tax was initially imposed as a means of funding war (1861), its original intent now combined with an element of wealth redistribution, lead to one of the most convoluted tax rate schedules of all time. The War Revenue Act of 1917 expanded the tax rate schedule from 7 to 56 tiers. Rates were hiked to a range of 6.0% to 77.0% in 1918. The 1918 tax rate schedule was so convoluted that taxpayers were thrown into a higher bracket with every $1,000 to $2,000 of additional income.

Although the war ended in 1918, income taxes were not significantly reduced until 1924. In 1919 the top rate was gradually lowered to 73.0%, then to 58.0% in 1922, and to 46.0% under the Mellon Tax Bill of 1924. By 1924, the tax rate schedule contained just 43 tiers compared to 56 in 1918. The bottom rate also gradually declined from 6.0% in 1918 to 2.0% in 1924. Then in 1925, under the leadership of President Calvin Coolidge, the bottom rate was reduced to 1.5%, the top rate slashed to 25.0% with a reduced top bracket, and the tax rate schedule was simplified to 23 tiers from 43.

In the midst of the Great Depression, President Herbert Hoover relapsed, imposing higher tax rates and expanding the number of tax brackets from 23 to 55. In 1932, the bottom rate was increased from 1.5% to 4.0%, and the top rate was hiked from 25.0% to 63.0%. Franklin Roosevelt would later increase the top rate to 79.0%, in 1936, where it remained through 1940. Hoover had in effect reinstated wartime tax rates during a time of peace. Errantly believing that higher taxes would increase government revenue, Hoover was the first president to prove that raising taxes during a recession only prolongs the downturn.

Thanks to Hoover, and his successor Franklin Roosevelt, the Great Depression wouldn’t end until America entered the 2nd World War. After Hoover opened the door, FDR removed the hinges, gradually raising rates from the bottom up. President Franklin Roosevelt believed and stated that, “Taxes, after all, are dues that we pay for the privileges of membership in an organized society.” This would mark a critical turning point in American history, as the purpose of the income tax had shifted from a temporary means to fund the Civil War, to a measure reinforcing lower tariff duties, to a tool for redistributing wealth, and ultimately to the price of living under the rule of a tyrannical dictator.

Following suit, bottom tax rates were raised from 4.0% in 1932, to 10.0% in 1941, to 19.0% in 1942, and to a record high of 23.0% in 1944. His successor, Harry Truman, would continue the tradition. After initially lowering the bottom rate to 20.0% in 1949, Truman raised it to 20.4% in 1951 and to 22.2% in 1952. The bottom rate was then locked in at 20.0%, by President Dwight Eisenhower, where it remained from 1954 through 1963. The top rate was likewise increased by FDR, climbing from 63.0% in 1932, to 79.0% in 1936, 81.0% in 1941, 88.0% in 1942, and to a record high of 94.0% in 1944 — during the height of the 2nd World War. Truman later lowered the top bar to 91.0% in 1946, and then raised it yet again to 92.0% in 1952. Eisenhower would fix the top tier at 91.0%, where it would remain from 1954 through 1963.

During the first 51 years after reinstatement of the income tax (1913 – 1963), the bottom rate commenced at 1.0%, peaked at 23.0%, and settled at 20.0%. Meanwhile, the top rate was nudged in at 7.0%, peaked at 94.0%, and ended the period at 91.0%. Imagine being in the top tax bracket with an opportunity to make an extra $1 million, and facing the prospect of handing over $910,000 of it to the government, while clutching to a paltry $90,000. Was that fair? Does it sound like a plan for economic prosperity and jobs growth? As we shall see, neither John F. Kennedy nor Ronald Reagan thought so.

The Tax Reduction Act of 1964

“Our tax system still siphons out of the private economy too large a share of personal and business purchasing power and reduces the incentive for risk, investment and effort – thereby aborting our recoveries and stifling our national growth rate.” – John F. Kennedy, Jan. 24, 1963, message to Congress on tax reduction and reform, House Doc. 43, 88th Congress, 1st Session

Finally in 1963, President John F. Kennedy was able to restore a measure of common sense to the overburdening income tax system. However, shortly after rebuking the “tax the rich” intelligentsia, JFK was assassinated in November 1963. He was succeeded by Lyndon Johnson who signed his vision into law. Under the Tax Reduction Act of 1964, the bottom rate was lowered from 20.0% in 1963, to 16.0% in 1964, and then to 14.0% from 1965 through 1976, and then later reduced to 0.0% in 1977 where it remained until 1986. The top rate was likewise reduced from 91.0% in 1963, to 77.0% in 1964, and then cut to 70.0% in 1965 where it remained until 1981.

Note: It was also during this era, that the Earned Income Credit (EIC) was signed into law by President Gerald Ford in 1975. The function of the EIC was to offset the burden Social Security taxes placed on low-income filers with children, and to motivate them to work.

In 1965 married couples with taxable income equivalent to $250,000 today paid a tax of 28.6%; those earning $1,000,000 paid 50.3%; and those earning $10,000,000 forked over 67.9% of taxable income (see table below).

During the entire 18 year period marking JFK’s tax reform legacy, married couples with taxable income equivalent to $250,000 today would have faced an average tax rate of 31.0%; those earning $1,000,000 would have paid an average rate of 52.8%; and those earning $10,000,000 would have forked over an average of 68.6% of their taxable income.

The Economic Recovery Tax Act of 1981

“We don’t have a trillion-dollar debt because we haven’t taxed enough; we have a trillion-dollar debt because we spend too much” ~Ronald Reagan – 40th US President (1981-1989)

In 1981, President Ronald Reagan, in the Jeffersonian spirit, with the wisdom of Lincoln, and the knowledge of Coolidge, took over where Kennedy left off. Summing up the folly of big government, he declared that, “The government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.” The Economic Recovery Tax Act, which went into effect in 1982, would maintain the bottom rate of 0.0%, and slash the top rate from 70.0% to 50.0%, but this was only the beginning.

In 1982 married couples with taxable income equivalent to $250,000 today paid a tax of 38.3%; those earning $1,000,000 paid 47.1%; and those earning $10,000,000 forked over 49.7% of taxable income (see table below).

The Tax Reform Act of 1986

The Economic Recovery Tax Act of 1981 was only a prelude to Reagan’s ultimate goal, tax reform. His objective was to simplify the income tax code, broaden the tax base and eliminate many tax shelters and other tax preferences. Under the Tax Reform Act of 1986 the bottom rate was raised from 0.0% to 11.0%, and the top rate slashed from 50.0% to 38.5%. As of 2011, the Act is the most recent major simplification of the tax code, drastically reducing the number of deductions and the number of tax brackets.

In 1987 a married couple with taxable income equivalent to $250,000 today paid a tax of 30.5%; those earning $1,000,000 paid 36.5%; and those earning $10,000,000 forked over 38.3% of taxable income (see table below).

The Tax Reform Act of 1986 culminated in the most simplified rate schedule since the days of Abraham Lincoln. Between 1988 and 1990, the tax rate schedule contained only two tiers, with a bottom rate of 15.0% for couples making under $56,504, and a top rate of 28.0% for those making $56,504 or more.

Between 1988 and 1990, married couples with taxable income equivalent to $250,000 today paid a tax of 25.1%; those earning $1,000,000 paid 27.3%; and those earning $10,000,000 had a tax liability of 27.9% of taxable income (see table below).

Although George H. W. Bush would ultimately raise taxes by adding a new top bracket of 31.0%, in 1991 through 1992, during the entire 11 year period, married couples with taxable income equivalent to $250,000 today would have faced an average tax rate of 30.5%; those earning $1,000,000 paid an average of 37.2%; and those earning $10,000,000 would have incurred an average tax liability of 39.3% of taxable income.

The Deficit Reduction Act of 1993

“I’ll tell you the whole story about that budget. Probably there are people in this room still mad at me at that budget because you think I raised your taxes too much. It might surprise you to know that I think I raised them too much, too” ~Bill Clinton – 1995

Bill Clinton’s Deficit Reduction Act of 1993 was nothing more than a tax hike. It was far from stellar, simply adding two new brackets above George H. W. Bush’s, but one positive aspect was that it represented a permanent change. The tax rates and brackets remained constant from 1993 through 2000, with an annual adjustment for inflation. The Act kept Reagan’s 15.0% and 28.0% brackets, and Bush’s 31.0% bracket in tact, and merely added two new brackets to the mix — 36.0% and 39.6%.

Note: Clinton is also responsible for implementing the Child Tax Credit, as part of the Taxpayer Relief Act of 1997. The credit was designed to provide tax relief to lower-income families. Initially, for tax year 1998, families with qualifying children were allowed a credit against their federal income tax of $400 for each qualifying child. For tax years after 1998, the credit increased to $500 per qualifying child, and for families with three or more children, the child tax credit was refundable.

During the 8 year period, 1993 through 2000, married couples with taxable income equivalent to $250,000 today enjoyed an average tax rate of 27.1%; those earning $1,000,000 incurred an average rate of 36.0%; and those earning $10,000,000 gave up an average of 39.2% of taxable income (see table below).

The Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA)

“He said, tax the rich. You’ve heard that before haven’t you? You know what that means. The rich dodge and you pay.” ~George W. Bush – 2004

In 2001, George W. Bush signed the Economic Growth and Tax Relief Reconciliation Act. The Act maintained the 15.0% bracket, and modestly reduced Reagan’s 28.0% bracket, Bush’s 31.0% bracket, and Clinton’s 36.0% and 39.6% brackets, to 27.5%, 30.5%, 35.5% and 39.1% in 2001. Then in 2002, the Act added a new 10.0% bracket (making it an authentic across the board tax cut), maintained a 15% bracket, and further reduced the remaining brackets to 27.0%, 30.0%, 35.0% and 38.6%.

Note: EGTRRA also enacted a stair-step schedule that raised the Child Tax Credit from $500 to $1,000 over a 10 year period. It also made a portion of the credit, known as the additional child tax credit, refundable.

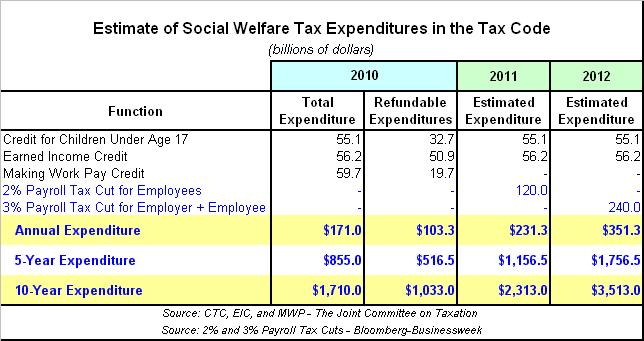

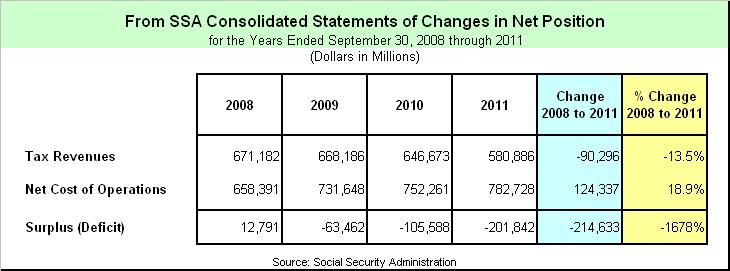

The following year, Bush would sign the Jobs and Growth Tax Relief Reconciliation Act of 2003 which provided the rates in force today. The Act maintained the 10.0% and 15.0% brackets, and reduced the remaining brackets to 25.0%, 28.0%, 33.0%, and 35.0%. As of today, although Barack Obama has delivered numerous speeches and proposed various temporary tax relief measures, such as a 2.0% cut on the employees’ portion of Social Security taxes (which threatens to accelerate the programs demise), he has offered nothing in the order of permanent tax reductions or reforms.

Between 2003 and 2011, married couples with taxable income equivalent to $250,000 today are accustomed to an average rate of 24.0%; those earning $1,000,000 have incurred an average of 32.0%; and those earning $10,000,000 are accustomed to paying an average tax of 34.7% of taxable income (see table below).

Pressing On

“Nothing in this world can take the place of persistence. Talent will not; nothing is more common than unsuccessful people with talent. Genius will not; unrewarded genius is almost a proverb. Education will not; the world is full of educated derelicts. Persistence and determination alone are omnipotent. The slogan ‘press on’ has solved and always will solve the problems of the human race.” ~Calvin Coolidge

When a taxpayer has enough deductions and credits to not owe any income tax, that should be the end of the matter, but that’s not the case today. No. Ever since enactment of the Earned Income Credit in 1975, followed by the Child Tax Credit in 1997, the federal income tax has become one of the government’s primary tools for the redistribution of wealth. Today, billions of dollars are transferred from one taxpayer to another before the funds ever reach federal coffers. Nowadays, a family with no tax liability at all may receive a “tax refund” of as much as $8,000 per year. This is most outrageous, and a matter which should be on the table for Congressional reform today, not tomorrow. In fact, on September 2, 2011, the Treasury Department’s Inspector General for Tax Administration reported that, in 2010, $4.2 billion in refundable credits were paid to individuals not even authorized to work in the United States. The federal government’s days of sitting around begging for more tax revenue, while recklessly giving away the dollars we currently pay are over.

When we examine the tax rates levied on upper incomes since the Revenue Act of 1913, we find that the average rate paid by married couples with taxable income equivalent to $250,000 today is 23.3%, while those earning $1,000,000 have paid an average tax of 38.6%; and those earning $10,000,000 have paid an average rate of 55.7%. The weighted averages are essentially the same, at 23.3%, 38.6%, and 55.8%, respectively (see table below).

But of course, if we take into account the first 137 years of American history prior to 1913, when the income tax was for the most part nonexistent, the historically weighted averages are actually significantly lower. We must never forget that out of 236 years of American history, the United States has only put up with an income tax for 110. That’s why many American’s are pressing towards a return to the low rates of Coolidge, while some long for the rates promised in 1913, and still others for repeal of the 16th Amendment.

Today we have Barack Obama, a man who seems curiously decoupled from any sense of American history. By repeatedly delivering the same broken record speech about raising taxes on millionaires and billionaires, while simultaneously proposing to apply the top tax rate to those earning $250,000, Obama has made himself the laughing stock of POTUS’. What gives? Did he miss the 1960’s, 1970’s, or 1980’s? Perhaps Obama was living outside of the country during a key decade, missing a segment of history that most Americans my age remember. I would suggest to Obama or anyone else proposing a radical change in U.S. tax policy, to first learn something about American tax history, and then proceed with caution. We must never forget that it was ‘taxation without representation’, an act of tyranny, which led to the first American Revolution.

Since 1913, the highest average tax rate assessed on taxable incomes of $250,000 has been 32.2%, during precarious times, the lowest 1.3%, and the historical weighted average 23.3%. So with that in mind, one can only imagine where Barack Obama is coming from as he delivers speech after speech hinting at raising taxes on millionaires and billionaires, a feat he portends to accomplish through ushering those making $250,000 into the top tax bracket. If we can learn anything from the past, it should be clear that tax rates on incomes of $1,000,000, $10,000,000 or more are lagging behind their historical weighted averages, while rates on those making $250,000 are within tolerance. So where’s the legislation spelling out the addition of upper brackets on those making millions and billions per year? Obama should either place a proposal in line with his rhetoric on the table, or simply step aside.

References / Related:

Taxing the Rich, Part I

Taxing the Rich, Part II

Spreadsheets: Historical Income Tax Data

Images: Tax Tables and Charts

Tax Foundation – Income Tax Tables: 1913 to 2011

Tax Acts of the United State, 1861 through 2010

The Origin of the Income Tax

Quick Revolutionary War Tour 1765-1777

#Taxes

CPI Adjusted Dollars:

http://www.measuringworth.com/uscompare/

http://www.dollartimes.com/calculators/inflation.htm