~ By: Larry Walker, Jr. ~

My previous advice proffered the simple concept of a

Mortgage in-Kind Exchange. If you didn’t like that notion, perhaps you will like this one. An Adjustable Principal Mortgage is a solution that would allow a mortgage company to temporarily write down the principal amount of a mortgage to an amount comparable to the contracts original debt ratio, and subsequently make adjustments every third year as home prices fluctuate. Once the value of the home equals or exceeds its original cost, no further adjustments are required. Neither the length of the loan or its interest rate is adjusted, nor may monthly principal and interest payments ever exceed the original amount.

An Adjustable Principal Mortgage would spread risk equally between mortgagor and mortgagee. When housing prices return to normal, both the lender and homeowner will have met their objectives; for the former a trustworthy return on investment and the latter a reasonable debt ratio. If housing prices continue to slump, mortgage companies and their investors will lose an amount comparable to the decline in value of the underlying asset, while homeowners losses are likewise mitigated. The value of all mortgage backed securities will be known at any point in time, rather than the present state of uncertainty. The idea is modeled after the Biblical proverb of the unrighteous steward.

The Unrighteous Steward ~ Luke 16:1-9

(1) “There was a rich man who had a manager, and this manager was reported to him as squandering his possessions. (2) “And he called him and said to him, ‘What is this I hear about you? Give an accounting of your management, for you can no longer be manager.’ (3) “The manager said to himself, ‘What shall I do, since my master is taking the management away from me? I am not strong enough to dig; I am ashamed to beg. (4) ‘I know what I shall do, so that when I am removed from the management people will welcome me into their homes.’ (5) “And he summoned each one of his master’s debtors, and he began saying to the first, ‘How much do you owe my master?’ (6) “And he said, ‘A hundred measures of oil.’ And he said to him, ‘Take your bill, and sit down quickly and write fifty.’ (7) “Then he said to another, ‘And how much do you owe?’ And he said, ‘A hundred measures of wheat.’ He said to him, ‘Take your bill, and write eighty.’ (8) “And his master praised the unrighteous manager because he had acted shrewdly; for the sons of this age are more shrewd in relation to their own kind than the sons of light. (9) “And I say to you, make friends for yourselves by means of the wealth of unrighteousness, so that when it fails, they will receive you into the eternal dwellings.”

It’s purely a matter of survival for homeowners, bankers, investors, the U.S. economy, and the nation as a whole. The unrighteous steward did what he had to do to survive. Presently, no one in the United States is doing anything to address the underwater vortex threatening to destroy the livelihood of millions of American homeowners. To date, the actions taken by both government and the private sector have done nothing to avert a looming global economic collapse and worldwide depression.

The Problem

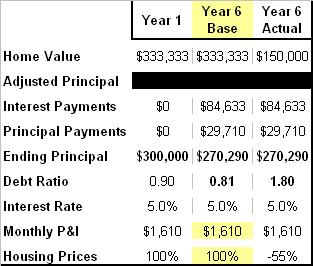

Jane is a 50 year old Georgia resident. She is married with two children. Jane purchased her home six years ago for $333,333. She initially made a down payment of $33,333 and took out a 30-year / 5% fixed rate mortgage of $300,000. She currently has an outstanding mortgage balance of $270,290, and the appraised value of her home has fallen to $150,000. If she were to sell the home today, she would incur a loss of $183,333, which is not deductible for tax purposes. Jane is not in default and can afford her mortgage payments, but one of the things bothering her is that her debt ratio, which started out at 0.90, has risen to 1.80. A debt ratio is calculated by dividing the amount of mortgage debt by the value of the home. A debt ratio of less than 1.0 is considered healthy, while a debt ratio greater than 1.0 is indicative of a loan at risk of default.

Jane feels cheated. By the sixth year, her debt ratio would have been 0.81, but for the decline in the value of her home. Her blood especially boils when she reads stories about homeowners cutting deals with lenders to stay in their houses literally for free, or of others who are in default yet have remained in their homes even after missing a year or two of payments. Jane has a bad, bad feeling that home prices won’t be improving within her lifetime, and fears that she may be foolishly throwing her money away. She would love for her mortgage company to reduce the principal balance of her loan, but that’s probably not going to happen, at least not until after a foreclosure.

So I will pose the same questions that I did last time, even though some of you took issue. “Does it make sense for Jane to sit there, stuck in a home that she can’t sell or refinance; making a payment every month on what she knows is a bad investment?” “Would you continue to invest $333,333 in an asset that you thought would be worth less than half in the future?” Although housing prices may rise over time, they didn’t reach their previous peak overnight, and life is finite. Jane is 50 years old, and doesn’t have another 30 years to waste. Since Jane doesn’t qualify for a loan modification, what options does she have? Presently, there doesn’t appear to be any solution other than to close her eyes, mask her feelings, keep paying, and go down with the ship.

Solution: The Adjustable Principal Mortgage

An Adjustable Principal Mortgage would allow the mortgage company to agree to temporarily write down the principal amount of a mortgage to an amount comparable to the contracts deemed debt ratio, and subsequently allow the principal to be adjusted every third year as home prices fluctuate. Once the value of the home equals or exceeds its original value, no further adjustments are required. Each time the principal is reset, it is re-amortized over the number of years remaining in the original term. The home is re-appraised at the end of each third year, and a new principal amount is calculated based on the ending debt ratio, multiplied by the current value of the home. At the end of the original term, any remaining balance is cancelled and the debt is considered paid in full.

The home may not be sold until its value equals or exceeds its original cost, without incurring a prepayment penalty. The penalty is calculated by subtracting the amount of all principal payments made to date, from the amount of debt owed prior to commencement of the Adjustable Principal Mortgage. In other words, anyone who opts out early will not be able to escape without having to make up the difference between the original debt and the adjusted principal. When the value of the home equals or exceeds its original cost, the homeowner may sell without penalty, paying off the balance at that time.

How it Works

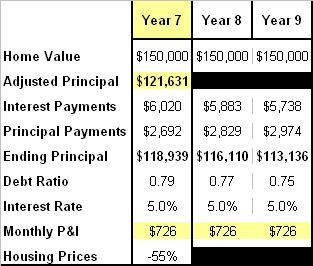

A home appraisal is required at the beginning of the term, and every third year thereafter. At the end of the sixth year, Jane’s home had a fair market value of $150,000 based on a 55% decline in value. That being the case, the principal amount of the loan is written down to what Jane’s debt ratio would have been in that year had her home not declined in value. In this case, had the home not lost value, Jane’s debt ratio would have been 0.81 (see ‘Year 6 Base’ in the table above). The principal amount of the loan is thus reset to $121,631 (150,000 * 0.81) [see note regarding rounding at the end]. Not only is the principal reset to $121,631, but the loan is re-amortized over a 24 year period (the original 30-year term minus the first 6 years). This results in a monthly principal and interest payment of $726 for the next three-year period.

Jane feels better already. There is no longer any reason to doubt. With her monthly payments reduced from $1,610 to $726, she now has an extra $884 to save or spend, both of which will help out her family and the ailing economy either way. At the end of the ninth year, Jane’s debt ratio is a healthy 0.75, and a new home appraisal is required. The new appraisal concludes that the home has increased in value by 50% to $225,000. Thus, the principal will be increased in the subsequent year.

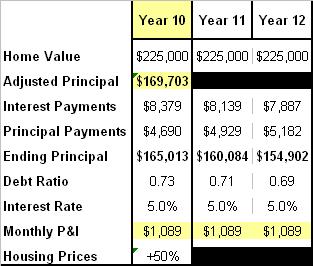

In the tenth year, the principal is raised to $169,703. This is calculated by multiplying Jane’s ninth year ending debt ratio of 0.75 by $225,000 (the current value of the home). The loan is then re-amortized over the remaining 21 years, resulting in a monthly principal and interest payment of $1,089 for the next three years.

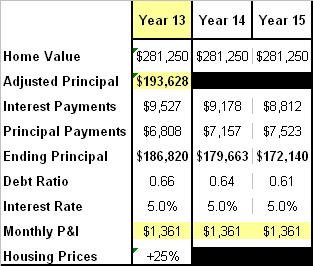

Although Jane would not be allowed to sell without incurring a prepayment penalty, she can see on paper that by the end of the twelfth year her debt ratio has declined to 0.69 with roughly $70,000 in home equity. Jane doesn’t mind the increased monthly payment because it is still lower than her original payment of $1,610, and because it was fairly determined based on the value of her home. At the end of the twelfth year the required appraisal determines that the home has increased in value by another 25% to $281,250, so the principal must rise again.

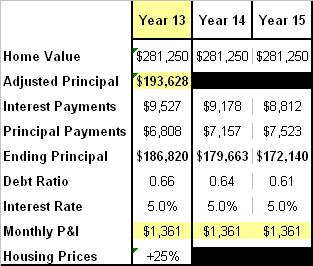

Since Jane’s debt ratio at the end of the twelfth year was 0.69, and the appraised value is now $281,250, the principal amount of the loan is stepped-up to $193,628 (0.69 * $281,250). The loan is re-amortized over the remaining 18 years resulting in a monthly payment of $1,361 for three years. Once again, Jane doesn’t mind the increase because she now has almost $110,000 in home equity, plus she is still paying less than her original payment.

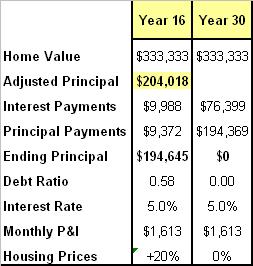

The required home appraisal at the end of the fifteenth year results in another 20% increase in valuation, making the home worth more than its original cost. Since the terms of an Adjustable Principal Mortgage cap any increase in valuation to the home’s original cost, the new mortgage principal is limited to $204,018. This is calculated by multiplying the debt ratio of 0.61 at the end of the fifteenth year by $333,333 (the original cost of the home).

In the sixteenth year, Jane’s adjusted loan principal of $204,018 is re-amortized over the remaining 15 years, resulting in monthly principal and interest payments of $1.613. Jane doesn’t mind this at all because her payments are essentially the same as they were under the original loan, plus she now has over $138,000 in home equity. The biggest bonus is that because her home has returned to its original value, Jane may now sell it free and clear at any time. If Jane keeps the home and it maintains an equal or greater value over the remaining 14 years, her monthly payments will remain $1,613, and her debt ratio will continue to decline.

In the example above, Jane is a winner. If I were her, I would quit while I was ahead by selling the home in the sixteenth year, but that’s her call. If she remains in the home for the full 30-year term, and if existing home prices continue to rise, Jane will have reached her original objective. Now let’s see what happens to the mortgage company.

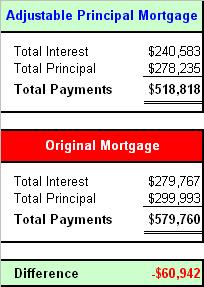

With an Adjustable Principal Mortgage, at the end of the 30-year term, the mortgage company will have earned $240,583 in interest income and will have recovered $278,235 of the original $300,000 principal. The reason that the principal repayments are short by $22,000 is because the mortgagor shrewdly wrote off a portion of the loan in order to keep the homeowner happy. The mortgage company still receives $218,818 over and above its original investment.

In comparison, had the terms of the original loan been fulfilled, the mortgage company would have received $279,767 in interest and the full amount of the principal. Overall the lender has given up $60,942 in interest and principal payments in order to help out a borrower whose underlying asset had declined by 55% in the sixth year of the contract. The alternative would be to risk foreclosure and an immediate loss, most likely in excess of $120,290 with the additional loss of interest income. In this respect, both the lender and borrower are winners.

Goals / Terms

-

Temporarily reduce the principal amount of underwater mortgages to the product of the homeowner’s target debt ratio and the home’s current market value.

-

Require a new home appraisal at the end of each three-year cycle.

-

Re-amortize the loan over the remaining life of the original term every third year.

-

Reset the principal amount of the loan every third year based on the homeowner’s ending debt ratio times the new appraised value.

-

The original length of the loan may not be increased.

-

The original interest rate remains fixed at the original rate and may not increase.

-

The value of the home may not exceed its original cost, for purposes of adjusting the loan principal.

-

Monthly principal and interest payments may not substantially exceed the amount of the original contract. Substantial is defined as meaning within $10 per month.

-

The homeowner may sell the home at any time, however if it is sold before reaching a valuation equal to its original cost, the homeowner will incur a prepayment penalty. The prepayment penalty is calculated by subtracting the amount of all principal payments made to date, from the amount of debt owed prior to commencement of the Adjustable Principal Mortgage. (Exceptions may apply where reasonable cause exists.)

-

Once the value of the home equals or exceeds its original cost, the homeowner may sell without penalty, only required to payoff the balance of the Adjusted Principal Mortgage.

Benefits / Costs

Lenders – By implementing the Adjustable Principal Mortgage lenders would potentially eliminate foreclosure losses such as may occur in the example above, multiplied millions of times over. If every underwater borrower decided to walk away tomorrow, it would spell the end of the mortgage industry, the end of the U.S. economy, and a sustained global depression. The costs of home appraisals, origination, and processing fees are passed on to homeowners. Although lenders will recover less than the amount stated in their original contracts, the amount forgone will be entirely based on how quickly home prices rebound, while failure to act would be catastrophic.

Homeowners – Borrowers will have a renewed confidence in the housing market. They will also receive the benefit of lower mortgage payments while their houses are underwater, allowing them to save or spend money that they otherwise would not have. This will result in an extraordinary amount of economic stimulus, at no cost to taxpayers. Homeowners will be responsible for the cost of home appraisals, loan processing and origination fees. Such fees may be paid for preferably out of pocket, or added to the principal.

The Economy – The resulting increase in economic activity will mean restoration of jobs for loan officers, administrative assistants, accountants, real estate appraisers, and others. By reducing the number of foreclosures, abandonments, and short sales, the housing market will improve. As real estate prices begin to stabilize and then increase, home builders and real estate agents will also return to work. Under a capitalist system there are winners and losers. Without changes everybody loses, but by taking action, by spreading the risk and by making the system fair, everyone’s a winner.

“And I say to you, make friends for yourselves by means of the wealth of unrighteousness, so that when it fails, they will receive you into the eternal dwellings.”

It’s time to implement solutions designed to solve real problems. While politicians have wasted time covering the loses of some private sector risk takers, lambasting others, and imposing more restrictive regulations, it has never once occurred to them to propose a real solution. Meanwhile, as private sector lenders have been mired in Congressional hearings, attacked with new regulations, and in many cases forced to accept government bailouts, they have likewise not taken time to resolve the real problem.

Note: All figures are rounded up to the nearest value. The approximation above is not intended to be a cure-all, it’s just an idea.

Data: Original Workbook