– War and Taxes: 1873 to 1963

– By: Larry Walker, Jr. –

“A wise and frugal government, which shall leave men free to regulate their own pursuits of industry and improvement, and shall not take from the mouth of labor the bread it has earned – this is the sum of good government.“ ~Thomas Jefferson

|

| From Taxing the Rich |

In the post-Civil War years, a booming economy produced tariff surpluses for decades. However, Democrat members of Congress, not wanting to give up on the pursuit of legalized theft, introduced sixty-eight income tax bills between the years of 1874 and 1894. It was in the midst of the Panic of 1893 that an amendment to the Wilson-Gorman Tariff Act of 1894 was passed, establishing a 2.0% tax on all incomes above $4,000 per year (about $104,000 today). The amendment would have exempted from taxation the salaries of state and local officials, federal judges, and the president.

Believing the income tax to be unconstitutional, President Grover Cleveland refused to sign it. The Act became law in 1894 without his signature, but was ruled to be unconstitutional in the following year. In 1895, the Supreme Court ruled 5-4 against the income tax, stating that its provisions amounted to a direct tax, which was prohibited by the U.S. Constitution. Prior to the 16th Amendment, a direct tax could only be levied if apportioned among the states according to the census, a concept that America could easily restore through its repeal.

Article I, Section 8: The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises, to pay the Debts and provide for the common Defence and general Welfare of the United States; but all Duties, Imposts and Excises shall be uniform throughout the United States.

Article I, Section 9: No capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or Enumeration herein before directed to be taken. [This section was changed in 1913 by passage of the 16th Amendment.]

Thus America remained the land of the free, free of income taxes from 1873 through 1912. But behind the scenes, the Democrat Party was fast at work, conjuring legislation which would ultimately destroy the freedoms won by Americans in 1776. Democrats proposed a constitutional income tax amendment in their party platforms of 1896 and 1908. Theodore Roosevelt endorsed both an income tax and an inheritance tax, and in 1908, became the first President of the United States to openly propose that the political power of government be used to redistribute wealth.

In 1909, the income tax amendment passed overwhelmingly in the Congress and was sent off to the states. The last state ratified the amendment on February 13, 1913. The Sixteenth Amendment owes its existence mainly to the West and South, where individual incomes of $5,000 or more were comparatively few. Sold to the public as mainly a tax on the rich, the income tax initially applied to less than 1.0% of the population, but that would be short lived. The aspirations of power hungry, greedy and wasteful politicians would soon change the federal government into the conundrum it is today.

“Government’s view of the economy could be summed up in a few short phrases: If it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.” ~Ronald Reagan

Those hornswoggled by today’s Democrat Party, having been indoctrinated in the tired old “tax the rich” mantra of the early 20th Century, will eventually find themselves mired in an infinite array of new taxes: energy taxes, excise taxes, higher Social Security and Medicare taxes, mandated health care taxes, consumption taxes, value added taxes, and every imaginable form of regressive fine and fee. From 1776 to the present, a battle has been waged to determine the government’s fair share of a private citizen’s earnings, and it will continue until government is finally restored to its Constitutional limitations.

The Revenue Act of 1913

In April of 1913, President Woodrow Wilson summoned a special session of Congress to confront the perennial tariff question. He was the first president since John Adams to make an appeal directly to Congress. Under the guise of reducing tariffs, the Act turned out to be nothing more than a means of reinstituting a federal income tax. The argument followed that since a reduction in tariff duties would lead to lost revenue, an income tax would be required to makeup the shortfall. We should be mindful of this as Barack Obama attempts to twist arms during his upcoming special session.

The 1913 Act appealed to those of the “tax the rich” mentality. Its progressive rates were similar to our modern day model, with the exception that it contained 7 tiers and a top rate of 7.0%, versus the present 6 tiers with a top rate of 35.0%. Marginal tax rates, under the 1913 Act, ranged from just 1.0% up to 7.0%. And since a married couple was allowed an exemption of $4,000, which was more than most people earned, most of the population was exempt. At the time, less than 1.0% of the population was subject to the tax, which helps to explain how the 16th Amendment achieved ratification: i.e. “It won’t affect me, so why should I care?” The largest proportion of the tax was targeted to those with incomes higher than anyone could imagine, as at the time, the top bracket of $500,000 was the equivalent of more than $10,000,000 today.

|

| From Taxing the Rich |

In 1913, a married couple with taxable income equivalent to $250,000 today would have paid a tax of just 1.0%; those earning $1,000,000 would have paid a tax of 1.6%; and those earning $10,000,000 would have incurred a tax rate of just 4.9% (see table below).

|

| From Taxing the Rich |

The War Revenue Act of 1917

World War I commenced on July 28, 1914 and lasted until November 11, 1918. Since the income tax was initially imposed as a means to fund war (1861), its original intent, now combined with an element of wealth redistribution, lead to one of the most convoluted tax rate schedules of all time. The War Revenue Act of 1917 expanded the tax rate schedule from 7 to 56 tiers. Rates were hiked to a range of 6.0% to 77.0% in 1918. The 1918 tax rate schedule was so convoluted that taxpayers were thrown into a higher bracket with every $1,000 to $2,000 of additional income.

|

| From Taxing the Rich |

Under the 1918 Act, a married couple with taxable income equivalent to $250,000 today would have paid a tax of 12.9%; those earning $1,000,000 would have paid a tax of 25.7%; and those earning $10,000,000 would have incurred a tax rate of 66.9% (see table below).

|

| From Taxing the Rich |

The Mellon Tax Bill (1924 – 1931)

Although the war ended in 1918, income taxes were not significantly reduced until 1924. In 1919 the top rate was gradually lowered to 73.0%, then to 58.0% in 1922, and to 46.0% under the Mellon Bill of 1924. By 1924, the tax rate schedule contained just 43 tiers compared to 56 in 1918. The bottom rate also gradually declined from 6.0% in 1918 to 2.0% in 1924. Then in 1925, under the leadership of President Calvin Coolidge, the bottom rate was reduced to 1.5%, the top rate slashed to 25.0% with a reduced top bracket, and the tax rate schedule was simplified to 23 tiers from 43.

Finally, common sense had returned. It was peacetime, and with taxes greatly reduced, the “Roaring Twenties” ensued. Although Coolidge didn’t cut top rates back to 7.0%, the lower rates he put in place, lasting from 1925 through 1931, have never been matched since. Coolidge had it right when he proclaimed that, “Collecting more taxes than is absolutely necessary is legalized robbery.”

|

| From Taxing the Rich |

Even before being elected President of the United States, the former Governor of Massachusetts understood and opined that, “There is a limit to the taxing power of a State beyond which increased rates produce decreased revenue. If that be exceeded intangible securities and other personal property become driven out of its jurisdiction, industry cannot meet its less burdened competitors, and no capital will be found for enlarging old or starting new enterprises. Such a condition means first stagnation, then decay and dissolution. There is before us a danger that our resources may be taxed out of existence and our prosperity destroyed.” ~Calvin Coolidge (Address to the General Court beginning the 2nd year as Governor of Massachusetts January 8, 1920)

By 1925, a married couple with taxable income equivalent to $250,000 today would have paid a tax of just 4.9%; those earning $1,000,000 would have paid a tax of 14.4%; and those earning $10,000,000 would have incurred a tax rate of 23.9% (see table below).

|

| From Taxing the Rich |

Revenue Acts of 1932 to 1940

In the midst of the Great Depression, President Herbert Hoover relapsed, imposing higher tax rates and expanding the number of tax brackets from 23 to 55. In 1932, the bottom rate was increased from 1.5% to 4.0%, and the top rate was hiked from 25.0% to 63.0%. The tax rate on upper brackets was later increased to 79.0%, by FDR, in 1936, where it would remain through 1940. Hoover had in effect reinstated wartime tax rates during a time of peace. Errantly believing that higher taxes would increase government revenue, Hoover was the first president to prove that raising taxes during a recession only prolongs the downturn. Thanks to Hoover, and his successor Franklin Roosevelt, the Great Depression wouldn’t end until America entered the 2nd World War.

|

| From Taxing the Rich |

In 1932, a married couple with taxable income equivalent to $250,000 today would have paid a tax of 8.6%; those earning $1,000,000 would have paid a tax of 21.8%; and those earning $10,000,000 would have forked over 54.8% of their taxable income (see table below).

|

| From Taxing the Rich |

Revenue Acts of 1941 to 1963

The next major tax hike would occur in 1941, with rates remaining at accelerated levels through 1963. After Hoover opened the door, FDR removed the hinges, gradually raising rates from the bottom up. President Franklin Roosevelt believed and stated that, “Taxes, after all, are dues that we pay for the privileges of membership in an organized society.” This would mark a critical turning point in American history, as the purpose of the income tax had shifted from a temporary means to fund the Civil War, to a measure reinforcing lower tariff duties, to the price of living under the rule of a tyrannical dictator.

Following suit, bottom tax rates were raised from 4.0% in 1932, to 10.0% in 1941, to 19.0% in 1942, and to a record high of 23.0% in 1944. His successor, Harry Truman, would continue the tradition. After initially lowering the bottom rate to 20.0% in 1949, Truman raised it to 20.4% in 1951 and to 22.2% in 1952. The bottom rate was then locked in at 20.0%, by President Dwight Eisenhower, where it remained from 1954 through 1963.

The top rate was likewise increased by FDR, climbing from 63.0% in 1932, to 79.0% in 1936, 81.0% in 1941, 88.0% in 1942, and to a record high of 94.0% in 1944 during the 2nd World War. Truman later lowered the top bar to 91.0% in 1946, and then raised it yet again to 92.0% in 1952. Eisenhower would fix the top tier at 91.0%, where it would remain from 1954 through 1963.

|

| From Taxing the Rich |

In 1941, a married couple with taxable income equivalent to $250,000 today would have paid a tax of 23.1%; those earning $1,000,000 would have paid 46.9%; and those earning $10,000,000 would have forked over 71.0% of their taxable income (see table below).

|

| From Taxing the Rich |

During the entire 23 year period, a married couple with taxable income equivalent to $250,000 today would have faced an average tax rate of 32.2%; those earning $1,000,000 paid an average tax of 57.6%; and those earning $10,000,000 would have forked over a whopping 85.5% of their taxable income (see table below).

Summary

“The government should create, issue, and circulate all the currency and credits needed to satisfy the spending power of the government and the buying power of consumers. By adoption of these principles, the taxpayers will be saved immense sums of interest. Money will cease to be master and become the servant of humanity.” ~Abraham Lincoln, 16th US President (1809-1865)

|

| From Taxing the Rich |

During the first 51 years after reinstatement of the income tax, from 1913 to 1963, the bottom rate commenced at 1.0%, peaked at 23.0%, and settled at 20.0%. Meanwhile, the top rate was nudged in at 7.0%, peaked at 94.0%, and ended the period at 91.0%. Imagine being in the top tax bracket with an opportunity to make an extra $1 million, and facing the prospect of handing over $910,000 of it to the government, while clutching to a paltry $90,000. Was that fair? Does it sound like a plan for economic prosperity and jobs growth? As we shall see, neither John F. Kennedy nor Ronald Reagan thought so.

The average rates on the wealthy during each significant wave between 1913 and 1963 are shown above. It is important to understand that a small imposition, upon the rich, blossomed into grand theft taxation. That’s what happens when citizens allow a government to act without restraint. Those seeking to usher couples with taxable income of $250,000 into the upper echelons of taxation should recognize that the highest tax rates ever assessed at this level, when wartime taxes were at a peak, averages out to 32.2%, while pre-1941 averages were below double digits.

It’s time for America to return to her roots. We cannot and will never again allow our government to lead us, as blind men, into the abyss. To raise taxes on one is to raise them on all. Those who believed they would always be exempt from taxes, in 1913, would soon find themselves paying nearly three times the rate initially assessed on the wealthy. Today, every worker is subject to Social Security and Medicare taxes totaling 15.3% (temporarily 13.3%), a rate which is more than double that paid by the wealthiest Americans under the Revenue Act of 1913. There is no escape; you’re either for higher taxes, or lower taxes. Don’t believe the lie. Those advocating higher taxes on the rich have always and will always ultimately raise them on every soul, from the bottom up.

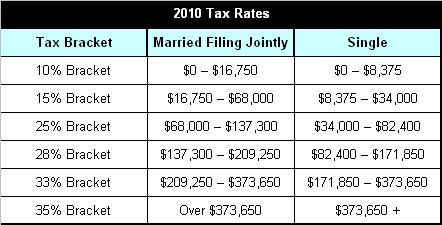

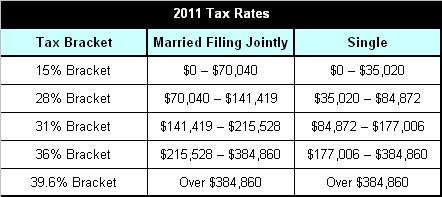

To be continued… Taxing the Rich – 1765 to 2011, Part III

References / Related:

Taxing the Rich – 1765 to 2011, Part I

Spreadsheets: Historical Income Tax Data

Images: Tax Tables and Charts

Tax Foundation – Income Tax Tables: 1913 to 2011

Tax Acts of the United State, 1861 through 2010

Quick Revolutionary War Tour 1765-1777

CPI Adjusted Dollars: