What Marketplace?

:: By: Larry Walker II ::

“Putting thoughts into words is vastly different from putting truth into words. For words are not truth. As ardently as writers sort and select and polish their words, at the end of the day they are still words. They are not, in themselves, truth…” ~ Lionel Fisher

The act of naming the federal government’s unlawfully subsidized website an “Exchange” or “Health Insurance Marketplace” doesn’t make it one. In a true marketplace, when a product or service is inadequate new competitors are allowed to step in and offer something better. But free competition is stifled when a government controlled, crony capitalist managed, overpriced monstrosity places rigid restrictions on the types of products and services offered. This is precisely the case with the health insurance plans offered by the U.S. government’s imaginary marketplace.

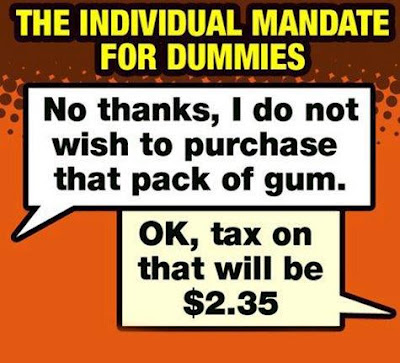

The federal government should do away with the individual mandate, including the vile affordable care excise tax, and open the “marketplace” to catastrophic plans. What kind of marketplace bars consumers from choosing between all possible options, and then imposes a tax for failing to make a purchase? That would be a government-run marketplace.

What is a Catastrophic Health Care Plan?

According to the federal government catastrophic health care plans are meant to provide protection from worst-case scenarios. They generally require you to pay all of your medical costs up to a certain amount (i.e. a deductible), which is usually several thousand dollars. Also according to the government, “they are basically the same as either not having insurance, or opting for a Bronze plan.” A statement that reveals something many have already discovered regarding the latter.

After reaching your deductible, costs for essential health benefits are generally paid by the plan. But here’s the key; catastrophic plans have lower monthly premiums than comprehensive plans. Although they primarily protect you from worst-case scenarios like serious accidents or illnesses, they also cover 3 primary care visits per year at no cost, even before you’ve met your deductible. They also cover free preventive services. Such features make them better than most comprehensive options.

As the law stands today, only U.S. residents under the age of 30 are allowed to purchase low-priced catastrophic health care policies. Those age 30 and over are out of luck, unless they have applied for and received a government approved hardship exemption. Those over the age of 30 aren’t even allowed to view the costs and benefits of such plans until they have obtained the burdensome bureaucratic sanctioned privilege.

Small Business Owners

Many Americans have money tied up in small businesses. The fact that some receive K-1 Forms from S-corporations or partnerships, reporting that they earned “X” amount of dollars, doesn’t mean they actually received a dime. Yet they are forced to pay income taxes on such earnings whether or not physically received. This is hardly fair, but now it’s worse.

If forced to remove all, or even a portion, of their earnings (or capital) from such enterprises each year, in order to comply with the Individual Mandate, many small business owners may not have sufficient funds to cover upcoming salaries, payroll taxes, debt service payments, general operating expenses, and income taxes. For these, catastrophic health insurance plans may be the best option.

Most Democrats are clueless about what I just said. Knowledgeable Democrats and unelected bureaucrats will say, “No problem, just fill out a 14 page hardship application, attach copies of your personal and business tax returns (and all other required backup documentation), and the federal government will get back to you and let you know whether or not you qualify for a catastrophic plan.” However, if a bureaucrat decides you can afford it, then you’ll either need to purchase an overpriced government approved plan, or pay the affordable excise tax.

The federal government doesn’t have a problem reducing any American to the level of a means-tested welfare program applicant, but resource allocation decision makers should. Are small business owners working 12 to 18 hour days to be treated like welfare applicants? I think not. They shouldn’t need a bureaucrat’s permission to purchase whatever type of health insurance meets their needs, and if none of the available options fit, they should be free to go without (i.e. free from a punitive excise tax).

Individual Market

If you’re single and think you might be able to afford up to $6,300 in medical bills each year (the bronze plan deductible for individuals), but are not sure you would be able to after having already forked over five thousand dollars (or so) in government mandated health insurance premiums upfront, you’re not alone.

If you’re married and not sure whether you could manage $12,600 in medical bills annually (the bronze plan deductible for couples), but are fairly certain you would not be able to after having been forced to pay ten thousand dollars (or so) in government-mandated health care premiums upfront, you’re not crazy.

Exorbitant health insurance deductibles, $6,300 for singles and $12,600 for families, coupled with pricey monthly premiums are precisely Obamacare’s problem, not to mention the unconscionable excise tax levied for noncompliance. The federal government may have forgotten that it already snatches 17% to 50% of its most productive citizen’s income each year, in the form of Social Security taxes, Medicare taxes, excise taxes and income taxes, but those affected by such and also subject to the Individual Mandate have not.

It’s been reported that middle class Americans, those most affected by Obamacare’s inflated premiums, are beginning to skip medical checkups and scrimp on their own health care, because once the premiums have been paid there isn’t much of anything left to cover the associated deductibles and out-of-pocket expenses dictated by an out of touch overlord.

Millions of middle class Americans don’t need to break their piggy banks trying to comply with the individual mandate, to know they would be forced to cut back on their own personal health care. After having wasted thousands of dollars a year to satisfy the Democrat Party’s seemingly drunken delusion, that every U.S. resident can afford health insurance, what they will be left with is a worthless insurance policy, not better health care.

To spell it out in terms anyone should be able to understand: Gross income minus federal and state income taxes, Social Security and Medicare taxes, rent or mortgage payments, utility bills, car payment(s), auto insurance, auto fuel and maintenance, debt service, food, clothing and personal expenses, retirement savings, and other family obligations, equals next to nothing for most of America. Yet, being well aware of this, the Democrat Party made the purchase of what it calls “minimum essential coverage” mandatory.

Quid Pro Quo

To better visualize the idiocy of Obamacare let’s compare it to a vehicle service contract and extended warranty. I recently purchased the package on a new vehicle. It covers the first five years or 60,000 miles for a one-time premium of $5,000. The cost was fairly steep, but what do I get in return?

When my truck needs an oil change, any regularly scheduled maintenance, or if any part fails, it’s covered. There are no deductibles or out-of-pocket costs. In other words, I don’t have to worry about shelling out another dime for nearly any situation which may occur with the truck over its first 5 years, or 60,000 miles. Not bad.

In comparison, an Obamacare bronze plan would cost me around $5,000, each and every year, subject to annual inflation increases. In addition, I would be forced to cover the first $6,300 I incur in medical expenses (the deductible), each and every year out of my own pocket. So over a five year period, I am expected to cover $25,000 in Obamacare premiums (subject to inflation), plus another $31,500 in out of pocket costs. Had this been the case with my truck, I would have bit the bullet.

Although a human being, at least in Western civilized society, is in theory worth more than a vehicle, that doesn’t mean a single middle class American can magically come up with $56,500 ($113,000 for a married couple), over a five year period, to comply with the Democrat Party’s pipe dream. Yet, for middle class taxpayers in their 50’s that’s what Obamacare demands. Let me check my bank book and see if I’ve got an extra $56,500 lying around from the last five years. What about you?

When it comes to getting something for something, that’s not what we find when it comes to the individual mandate. Thanks, but I’ll take a pass on Obamacare. Anyone that thinks this is a rational plan was either already covered by a governmental or employer health care plan, or is pitifully out of touch with reality. But this is always the case with big government programs run amok. Unless a program affects people in a personal manner, most tend to be idealistic or apathetic.

Fixing Obamacare

As revealed in Part III, in spite of Obamacare, 30 million U.S. residents are projected to remain uninsured indefinitely. Among them, 26 million are expected to claim an exemption from the penalty. Did I say penalty? Sorry, I meant excise tax. In its present form, the law is without question a colossal failure, and ignoring the results of the most recent landslide election would be a monumental miscalculation.

Government intervention in the health insurance market, in the form of excise taxes, tax credits, subsidies and regulations has led to the unintended consequences of artificially high insurance premiums and lofty deductibles. Imposing an excise tax on consumers least able to comply with the mandate, forcing them to choose between purchasing an overpriced policy or paying a tax, has created another unintended consequence – animosity toward one’s own government.

How can we amend this broken concept?

-

The federal government should simply drop its individual mandate and let the market operate freely. That means no subsidies and no excise taxes.

-

Then, it should allow anyone desiring to purchase a catastrophic health insurance policy the right to do so, regardless of age or household income.

Any hope of reducing costs, restoring national allegiance, and encouraging the uninsured to enter (or reenter) what used to constitute a health insurance marketplace rests on this combination. If the federal government is sincerely concerned with the welfare of all of its citizens and residents, it will repeal the individual mandate and establish a true marketplace.

The End; hopefully of Obamacare.

Related:

Affordable Care Excise Tax, Part I

Affordable Care Excise Tax, Part II

Affordable Care Excise Tax, Part III

Picture credit: Emergency Physicians Monthly