– 6 Temporary Stimuli, 17 Tax “Cuts”, and Zero Results

– By: Larry Walker, Jr. –

As I carefully chronicled in, “Obama: The Era of Flimflam Economics, Part II – Untimely and Proven to Fail”, the policy theory, known as economic stimulus, was designed by economists as a tool for implementation at the onset of a recession, with the goal of either softening its effects, or averting a downturn altogether. However, in the real economy, economic stimulus has yet to be proven successful at doing either. In February of 2009, partisan windbag, Barack Obama declared, “What do you think a stimulus is?“, implying that the idea was for the government to borrow and spend near a trillion dollars on anything, but then later at a Jobs Council, after the money had been squandered, he admitted that, “Shovel-Ready Was Not as Shovel-Ready as We Expected”.

Short-Term Stimulus vs. Long-Term Policy

To summarize, it was near the end of 2007, when prominent economists began advising the federal government that the economy was heading into a recession, and that it could be avoided if the government would implement an economic stimulus program. They proffered that in order to work successfully, such a stimulus needed to be targeted, timely, and temporary. As far as timeliness was concerned, tax refund checks needed to reach taxpayers in a matter of weeks not months. But economists must have forgotten that they were dealing with the federal government. How in the world would the federal government be able to: (1) agree on and pass legislation, (2) send it on to the IRS for interpretation and implementation, and (3) expect for tax refund checks to start rolling out in a couple of weeks, especially in the middle of the tax filing season?

The first economic stimulus package of the Great Recession was proposed in January of 2008. Even though a similar stimulus plan was attempted and failed in 2001, nevertheless, Congress was suckered in through panic mode once again. This time they would fling $150 billion to the wind, but by the time the checks reached taxpayers, in April of 2008, it was too late, the recession had commenced. Looking back, it turns out that the recession officially commenced in December of 2007 and didn’t end until June of 2009. So why is it that millions of job losses, millions of home foreclosures, hundreds of bank failures and trillions of dollars in government debt later, politicians still seem to be hell bent on the premise that temporary stimulus policies work?

In February of 2009, a year after the first failed tactic, Barack Obama enacted a second stimulus plan. The American Recovery and Reinvestment Act of 2009 turned out to be nothing more than a gigantic, nearly $1 trillion, spending program. Although his borrow-and-spend policy was designed to be temporary, it was neither targeted nor timely. So the questions then and now are: Why was the federal government still trying to implement a stimulus program 14 months after the recession began, when every honest economist knows that the idea is to inject stimulus either prior to or just as a recession commences? By February of 2009, was it possible for a stimulus plan to prevent something which had already occurred? And lastly, why is the federal government still toying with the idea today, some 27 months after the recession has ended?

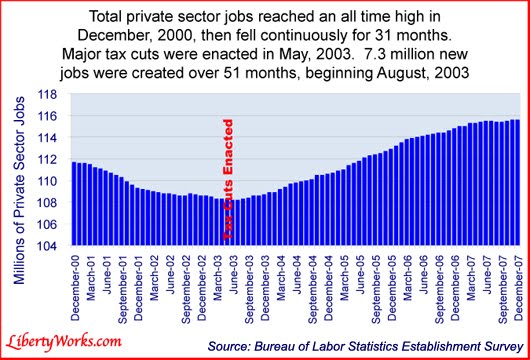

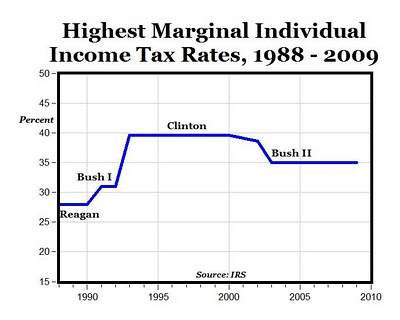

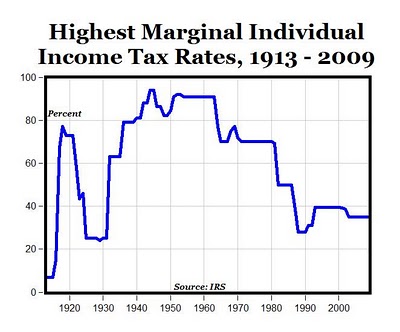

It should be rather obvious by now that economic stimulus programs don’t work in the real world. Although the theory may look impressive on a chalk board, the federal government is not an efficient institution for implementing a positive jolt to the economy, let alone much of anything else. It should also be clear that there are economic recovery policies which have been proven to work, time immemorial, once a recession has passed. For example, The Tax Reduction Act of 1964, The Economic Recovery Tax Act of 1981, The Tax Reform Act of 1986, The Deficit Reduction Act of 1993, and the Jobs and Growth Tax Relief Reconciliation Act of 2003 were all long-term plans which stabilized and grew the economy following recessions.

What’s lacking today is a long-term tax policy which would inject a sense of stability and predictability to the economy at large. Small businesses don’t make plans based on hope and change, what we need is to know what our income tax rates and incentives will be for the next 8 to 10 years. Yet, Obama has wasted nearly 3 years already, passing one temporary measure after another, and now it’s more of the same. As far as I’m concerned, it’s over for Obama. With the knowledge that long-term tax policies have been used as effective recovery tools following recessions, and that short-term stimulus programs have never been successful, why in the world is Obama trying to subject the nation to another stimulus prototype now, some 3 years and 9 months after the Great Recession began? Is it because we’re on the verge of another recession? And if we are on the verge of a double-dip, knowing that temporary stimulus programs don’t work in the real world, why would we ever allow Obama and Congress to waste more time, and money that we don’t have, with yet another futile stab?

From Main Street to Washington, DC

Having been an accountant and tax advisor for many small businesses, including my own, through at least the last two recessions, I know first hand which tax policies have worked and haven’t, and which have been important to small businesses versus the completely useless. For example, after passage of the Jobs and Growth Tax Relief Reconciliation Act of 2003, there was a sense of stability, and future plans could be implemented without the lingering fear that something would change or be taken away the following year. Its key policies which helped small businesses, within my orbit, were as follows:

-

Stable and well defined Personal and Corporate Income Tax Rates and Brackets.

-

Accelerated Depreciation through Section 179 and Bonus Depreciation within clearly defined limits and timeframes.

-

Increasing and well defined limits on IRA and Qualified Retirement Plan contributions.

-

Stable and declining tax rates on capital gains, and qualified dividends.

-

Defined and stable tax credits such as the energy efficiency credit, child tax credit, education credit, and the life-time learning credit.

-

Stable, declining and well defined Estate tax rates and brackets.

In contrast, the policies I have witnessed since February of 2009, have made planning next to impossible and pretty much pointless. For example, we knew that the tax rates and most of the policies implemented by #43 would expire at the end of 2010, so that was pretty much the end of the planning cycle, however the recession cut many plans short well before 2010. In fact, many small businesses didn’t make it through 2008, and some went under in 2009. As for the survivors, well what we’ve all been waiting for are the permanent policies which will carry us through the next decade. But thus far, all we’ve seen is a series of temporary tax measures, many with erratic nonsensical start and end dates, and most of which have been completely useless at a time when gross business income has for the most part been depressed.

Obama’s 17 Phantom Tax Cuts for Small Business

Obama has implemented 17, so called, tax cuts for small business. For the complete list, see the Feb. 25, 2011, posting on the official White House blog entitled, “Seventeen Small Business Tax Cuts and Counting.” The post is touted as enumerating 17 small business tax cuts and credits created or extended through legislation signed by Obama, since February of 2009. But what is important to remember is that it’s not how many tax cuts have been implemented, but rather, whether or not they have been effective. Overall, I would have to give the Obama policies a grade of “D”. Obama’s 17 small business tax policies (or as he calls them “cuts”), and their effectiveness from my point of view follows, but first, here’s a short summary:

-

Eight of them were included in American Recovery and Reinvestment Act (aka the economic stimulus), the Affordable Care Act (aka the health care law), and the Hiring Incentives to Restore Employment Act (aka the Hire Act). Among the cuts: the exclusion of up to 75 percent of capital gains on key small business investments; a tax credit for the cost of health insurance for small business employees, and new tax credits for hiring Americans out of work for at least two months.

-

Another eight came via the Small Business Jobs Act, signed by President Obama in September of 2010. These included: adding deductions for business cell phone use; creating a new deduction for health care costs for the self-employed; allowing greater deductions for business start-up expenses; eliminating taxes on all capital gains from key small business investments, and raising the small business expense limit to $500,000.

-

Three months later, he signed a tax bill that raised the expense limit to 100 percent of small business new investments until the end of 2011. It also extended the elimination of capital gains taxes for small business investments through the end of 2012.

From the Recovery Act, HIRE Acts, and Affordable Care Act

1. A new small business health care tax credit

We didn’t have any businesses qualify for this credit. The calculation was very complex, so it wasn’t readily known whether any businesses would qualify until after the end of the tax year. It’s kind of difficult to shoot for something when even your accountant says, “I don’t know. I’ll let you know as soon as the IRS puts out some regulations showing us how it will be calculated.” And then well into the following year, “I’ll get back to you as soon as the IRS releases the appropriate tax forms.” One business came close to qualifying, but the employees’ salaries turned out to be too high. Who knew?

The small businesses I deal with don’t normally determine what their employees salaries and benefits will be based on temporary government policies. And they don’t sit around waiting on the IRS to publish forms and regulations when a decision is needed right away. In other words, when a business needs 4 more engineers, due to demand, negotiations don’t center on keeping salaries below a certain threshold in order to qualify for a one-year, one-time tax credit. And negotiations for health care plans center more on the affordability of monthly payments, and are not recklessly entered into with the hope of receiving a one-time tax credit, to be realized in some subsequent year.

Most small businesses in my sphere don’t offer health insurance, simply because it’s cost prohibitive, so the idea of a one-time tax credit, to offset the cost of something unaffordable to begin with, turned out to be pretty much a waste of orating skills, paper and ink. It sounded good though, and I guess that’s what counts with Obama and his cronies.

2. A new tax credit for hiring unemployed workers

I would say three businesses may have qualified for this credit, and mostly by luck. Others thought they would qualify, but it turned out that the new hires had not been unemployed for at least 60 days which disqualified them. I got lucky by hiring someone who had been unemployed for more than 60 days, and was luckily hired a few days after the law went into effect. But it wasn’t like I was hunting for someone who would qualify, and didn’t even know about the credit at the time because the details were not readily available. Again, I don’t know of any small businesses that hire people based on temporary tax credits, most hire people when they are needed to meet the objectives of the organization.

Also, since our payroll tax software wasn’t set up to account for the credit, because it was implemented after the start of the tax year, and since IRS Form 941 was not updated when the credit went into effect, it turned out to be more of an accounting nightmare than anything else. Personally, I would have gladly forgone the credit in exchange for not having to figure out how to account for it. Thank God that’s over with. Can we please just have some stability so we can run our businesses without something changing every few months?

3. Bonus depreciation tax incentives to support new investment

Section 179 depreciation has generally been sufficient. Although, bonus depreciation is advantageous at times, it’s more advantageous when a business has a loss, which is generally not the goal. If net income is high enough to write-off all equipment purchases, why would anyone choose to write-off half? Like I said, there is an application, but it mostly applies when net income equals zero, and one wishes to accelerate a loss. There were a few takers, but come to think of it, most of those went out of business due to the losses already incurred.

Uncertainty – From a planning standpoint, the other looming question was that, if the Bush tax cuts were going to expire at the end of 2010, might the depreciation expense perhaps be better utilized in the year rates were set to increase rather than while rates were low? Thus it may have made more sense to just delay any purchases until 2011, or 2012 rather than accelerate the write-offs while tax rates were still relatively low. Again, a stable long-term tax policy trumps temporary measures any day.

4. 75 percent exclusion of small business capital gains

This was of no use whatsoever from my vantage point. One would have to purchase qualified small business stock after February 17, 2009 and before January 1, 2011, and then hold it for five years in order to take advantage. None of our small businesses make a living through buying and selling small company stock. The only practical use I could see was for owners planning to sell their stake in a company, but they would have had to acquire that stake between the dates above, so it wasn’t much use to existing business owners. My first impression was that it was a policy designed for those looking to make a quick exit and perhaps relocate overseas, but the five year hold time destroyed that dream. If you’re interested in how convoluted this provision turned out to be, there’s an interesting article here.

5. Expansion of limits on small business expensing

Did anybody in Washington, DC get the memo that surviving small businesses just got hammered for two years straight, and thus had no money left, and no desire to go out on credit for new equipment, if credit could even be obtained? All I can say is that the old limit of $25K seemed to be more than sufficient to cover replacement items. I haven’t witnessed any considerable expansion plans since 2006.

Uncertainty – From a planning standpoint, the other looming question was that, if the Bush tax cuts were going to expire at the end of 2010, might the depreciation expense perhaps be better utilized in the year rates were set to increase rather than while rates were low? Thus it may have made more sense to just delay any purchases until 2011, or 2012 rather than accelerate the write-offs while tax rates were still relatively low. Again, a stable long-term tax policy trumps temporary measures any day.

6. Five-year carryback of net operating losses

This was yet another policy more useful for those who lost money and were on their way out of business, than for those fighting but keeping their heads above water. I took this as more of a policy of defeat than future success. I guess the government figured that a small tax refund from five years ago would encourage small businesses to keep hiring while losing money in the meantime. I had a couple of businesses utilize the five-year carryback, but unfortunately they are no longer in business.

7. Reduction of the built-in gains holding period for small businesses from 10 to 7 years to allow small business greater flexibility in their investments

This was another waste of paper and ink. This policy only helped out S-Corporations who were formerly taxed as C-Corporations, and had built in gains at the time of conversion. A built in gain is the difference between the fair market value of an asset and its tax basis at the time of the conversion. I’m sure some businesses out there took advantage, but really, how many C-Corporations switched to S-Corporation status? I think I advised one to do it maybe 10 years ago, but other than that it hasn’t always been the best move due to built-in gains, undistributed net profits, the number of shareholders, or the owner’s personal tax situation. The majority of the small businesses in my neck of the woods have been S-Corporations from inception, generally based on my advice. So did anyone actually benefit from this provision? I have serious doubts.

8. Temporary small business estimated tax payment relief to allow small businesses to keep needed cash on hand

Since estimated tax payments are made throughout the year in order to reduce or eliminate the amount owed when the tax return is due, the full amount being due by March 15th, why would I advise any small business to skimp? I had no takers here either. Most small business owners who make estimated tax payments want their taxes covered by tax time, and don’t want to skimp on estimated tax payments during the year, and then get stuck with a gigantic tax bill later. If a business took advantage of this and then didn’t have funds to pay on March 15th it would only snowball into perpetual tax debt. ‘Once you get behind, you never catch up.’ So this was another waste of paper and ink. Hey, do we look stupid or what? Why not just cut the doggone tax rates, and stop playing games?

From the Small Business Jobs Act

9. Zero capital gains taxes on key investments in small businesses

Zero is right! Like I said in number 4 (above), it was of no use whatsoever when 75% of the gain was excluded, from my vantage point. To slip through this loophole, one would have had to purchase qualified small business stock after September 27, 2010 and before January 1, 2011. Since there were only three month’s to gear up, and it was the holiday season, I’m pretty sure no one took advantage, but if you did, please shout it from the rooftops. None of our small business clients make a living through buying and selling small company stock. The only practical use I could see was for an owner planning to sell their stake in the company, but to gain any benefit, they would have to acquire that stake between the dates above, and so it wasn’t much use to existing small business owners. My first impression was that it was a policy designed for those looking to make a quick exit and perhaps relocate overseas, but the five year hold time once again destroys that dream. This was another waste of paper and ink. If you’re interested in how convoluted this provision turned out to be there’s an interesting article here.

10. Raising the small business expensing to $500,000

I didn’t have any small business clients who were able or desired to purchase anywhere near $500K of new equipment. Since this doesn’t apply to real property, it’s generally well beyond the needs of most of the small businesses in my area. Thus, I had no takers. This might be a great policy for well capitalized startup businesses, but the number of startups has been on the decline, and most that I know of haven’t had that much capital. Since the write-off is limited to a businesses net income, $500K is generally beyond the earnings of most first year enterprises. This is generally a good policy to implement in the middle of a recovery in order to maintain growth, but not in the midst of a weak economy. Thus to me, it amounted to another waste of paper and ink.

11. An extension of 50 percent bonus depreciation

Hey, didn’t we try this already? See number 3 (above).

12. A new deduction for health care [insurance] expenses for the self-employed

This is actually a bit misleading. It should read ‘deduction for health “insurance” expenses’, not ‘health “care” expenses’. Since most of the small businesses we advise are S-Corporations, owner-employees with company paid health insurance, were already allowed a 100% deduction for health insurance long before this Act. The amount paid is included in their wages, but not subject to Social Security and Medicare taxes, and is allowed to be written off in full on their personal returns. This results in a total offset on the personal return, and a higher wage deduction on the S-Corporation return. I suppose it helped some sole-proprietors, Schedule C filers who have health insurance, but it didn’t affect anyone within my practice. Why walk when you can fly?

13. Tax relief and simplification for cell phone deductions

Most small businesses actually using cell phones for business purposes were already deducting the business usage portion. This provision only helped to avert a threatened crack down on the deduction which would have made it more costly to maintain records proving every call was business related, but since the crackdown never occurred, the effect upon small businesses was a sigh of relief, but no additional savings. In other words it saved us from having to spend more to comply with yet another ridiculous government regulation, but was really just a wash. Nothing was really saved, and nothing gained, in other words, it may have sounded good, but the effect was nil.

It’s akin to the government making 1099’s mandatory for all vendors, cancelling the regulation before implementation, and then claiming to have saved businesses money. No. You didn’t save us money. What you did was give us two years of uncertainty and unneeded stress, that’s what you gave us. That’s why government should just get out of the way.

14. An increase in the deduction for entrepreneurs’ start-up expenses

Although this policy temporarily increased, in 2010, the amount of start-up expenditures entrepreneurs could deduct from their taxes from $5,000 to $10,000, most of the start-up expenses that come across my desk are in the $100’s not thousands. And in cases where there are larger amounts, but little initial year net income, taking the write-off over 60 months is sometimes more plausible, especially when one doesn’t know whether tax rates will be higher in subsequent years, which by the way, we still don’t know.

15. A five-year carryback of general business credits

This policy allowed certain small businesses to “carry back” their general business credits to offset five years of taxes. I didn’t have any business clients qualify for any of the general business credits last year, and none who were really targeting them. In fact, the last business I can remember taking advantage of one of these credits was advised to do so through a tax scam. They paid the scammer an upfront fee in same amount as the credit they were assured to get back from the IRS. But in the end, all they got was an IRS audit resulting in the disallowance of the credit, had to pay the IRS back, and then had to sue the scammer to be made whole. I’m sure there are legitimate uses for some of these credits; I just haven’t dealt with any small businesses lately where any of them would have made a difference. You may view a full list of the credits here. In my view, most are either obsolete, redundant, or serve only a narrow base of special interests. Anyone serious about tax reform has my permission to strike the entire list.

16. Limitations on penalties for errors in tax reporting that disproportionately affect small business

The bill would change the penalty for failing to report certain tax transactions from a fixed dollar amount – which was criticized for imposing a larger penalty on small businesses – to a percentage of the tax benefits from the transaction. There was a time that all tax penalties were based on a percentage of taxes owed, but that’s no longer the case. Unfortunately this new provision doesn’t limit the effect of the $195 per month penalty the IRS currently charges, per shareholder, for each part of a month that an S-Corporation or Partnership return is filed late. S-Corporations and Partnerships, which have no income tax liability, are currently assessed the penalty, even though the late filing typically affects only a limited number of owners, or sometimes just one. If the government was serious about helping small businesses, they would stick to the old percentage of tax benefit policy (i.e. no tax benefit, no penalty), and eliminate this unfair charge on small businesses immediately.

And from the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act

17. 100 percent expensing

Hey, didn’t we do this twice already? See numbers 3 and 11 (above). This provision only applies to qualified property placed in service after September 8, 2010 and before January 1, 2012. So for those who purchased qualifying equipment on or before September 7, 2010, too bad, you should have waited. This is a prime example of another wacky implementation date from Obama. It’s also the provision that allows up to 100% of the price of an SUV or Corporate Jet to be written off in the first year, a provision signed into law by Obama, who later railed against the same.

This might be a good thing for some, but so far we haven’t seen any great demand for purchasing new equipment, no matter the incentive. Most small businesses, within my scope, are trying to pay off the debt from yesteryears purchases, and not looking to expand, or to replace equipment unless it’s an emergency. In other words, it’s not just hiring that’s down, it’s the economy as a whole, and with that comes dealing with slow paying customers, managing debt, grappling with price competition, and cutting back on expenses – including the purchase of new equipment. Thus, upping bonus depreciation from 50% to 100% looks good on paper, but it’s another temporary measure which in my estimation will not provide the spark needed to boost the economy.

Conclusion

Overall, most of Obama’s so called tax “cuts”, listed above, may make good sound bites, but I haven’t found them to have much practical application in the real world. There was a time, not so long ago, that the term tax cut, meant exactly that. It meant that tax rates were reduced. None of the provisions above represent reductions to income tax rates or adjustments to tax brackets, so they are not technically tax cuts. They are merely temporary ploys, targeting special interest groups, requiring one to either borrow and spend money, or jump through unreasonable (often impossible) hoops simply to obtain an additional deduction or credit.

Meanwhile, on Main Street, a permanent reduction in personal and corporate income tax rates, from the get go, would probably have had a greater impact, even if it were done in stages, with super low rates for two years followed by modest increases over the next eight, or something. None of Obama’s 17 tax deductions, credits, or extensions have really mattered much to me or to most of my small business clients, and the stuff he’s talking about now won’t make much of a difference either. If it’s temporary, and if it requires jumping through hoops, borrowing money, or meeting time frames beginning in the middle of the year – or starting on some arbitrary date in some odd month, then just forget it. It would be a heck of a lot easier to just cut overall income tax rates for one year, and then provide fixed rate schedules for the next decade. Is that so difficult? Is it really? If JFK, Reagan, Clinton, and ‘W’ could do it, why couldn’t Obama?

It’s all over for Obama now, time to move on. He had his chance, and blew it. The era of temporary stimulus boondoggles is over. Instead of thinking targeted, timely and temporary, it’s time to move towards a plan that’s broader based, strategic and permanent. Now it’s up to Congress and the 2012 presidential candidates to outline a long-term strategy and take it to every corner of the country.

References:

DNC Chair Wasserman Schultz says Obama has signed bills with 17 small business tax cuts