A Fiscal Conservative Opines: Where is all the excess?

By: Larry Walker, Jr.

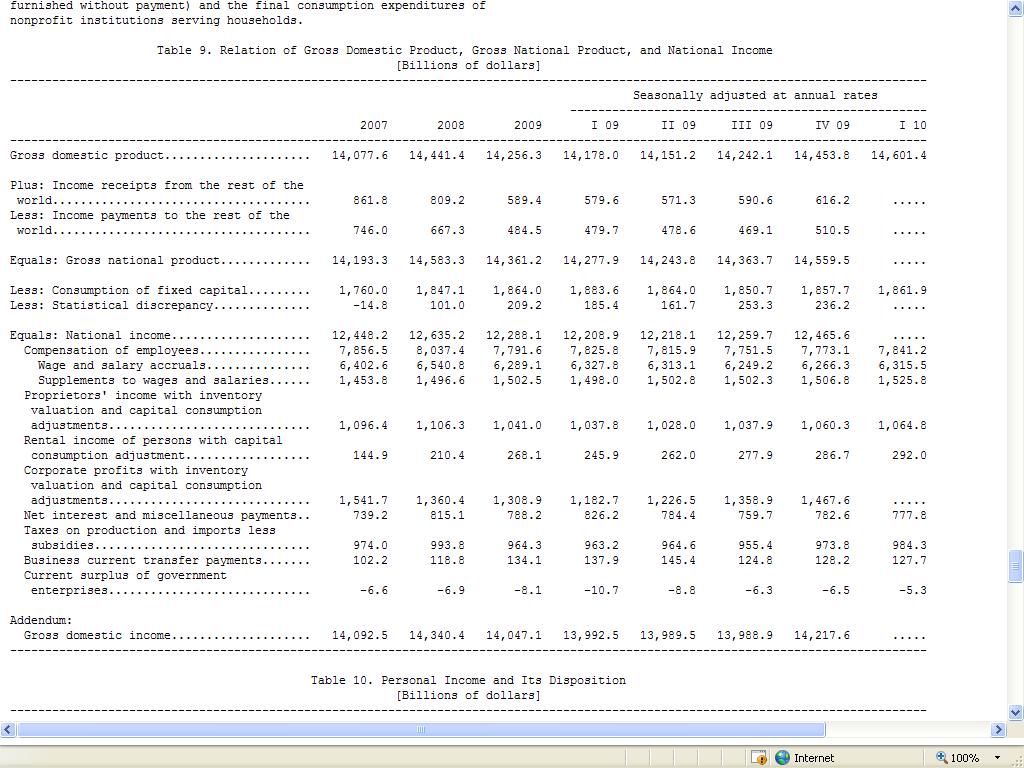

I am once again attempting to overlay data upon data from different sources, not being certain whether any of them are accurate, yet they are all so called ‘reputable’. There are some who will look at the table, above, and think that health care expenditures are out of control. I look at it and my take is that the lack of growth in real incomes is the problem.

In fact, health care expenditures have been on the decline since 2003. Granted I was not able to find the rate of change for 2009, even if there was no increase, health care expenditures have grown faster than incomes, the consumer price index, and GDP. This doesn’t tell me that there is necessarily a problem with health care expenditures. What it tells me … is that there is a problem with the economy.

Over the past ten years, consumer prices have risen by 25% while incomes have only risen by 9%. Does this mean that prices are out of control? Not to me. To me it means that our incomes are not keeping pace with inflation.

GDP is growing slower than prices. GDP is only growing at an average of 1.9% per year. For the past decade, GDP grew by 19% while prices grew by 25%. So again, is the problem with prices, or with GDP?

Let’s be real. Unless prices rise, incomes will not. How can a business provide raises for employees every year unless the business is also raising its prices? One way would be to keep prices static and to increase productivity, which generally means doing more with less employees. Everyone expects to get a cost of living increase each year, however, in order to receive one, your employer must generally raise its prices in line with the consumer price index. Yet, if that was reality, then incomes would be rising as fast as inflation. Yet, prices have risen nearly three times as fast as incomes. So where is all the excess?

My suspicion is that the problem lies more in the area of manufacturing, international trade, unionization, and the growth of government. We don’t make things anymore in America, we have become a service economy. Most of the products that we buy are imported from other countries. Unions are constantly demanding higher wages and better benefits. The number of government employees is growing as is their pay and benefits. The end result is that our Federal and State governments are going broke, jobs are being lost to emerging market economies, and the incomes of non-governmental and non-union employees are going down.

So the question is how do we improve the growth prospects for our economy? The answer lies in finding ways to increase exports and decrease imports, to lower income taxes and reduce the size of government, and to remove the restraints currently being imposed upon the free market. Our economy doesn’t need more controls, but rather less.

You say rising health care costs are at the center of all of our problems. I say, you’re focusing on the wrong statistic. If a man or woman has no way to earn their livelihood, then what good is a government run health care program. You will have your health care, but you will live in poverty. You will be taxed, but you will lack the wherewithal to pay your taxes. The poor will remain poor. The middle class will cease to exist. The government will continue to spend more than it can tax until even it falls by the wayside.

You cannot fix a problem, until you have identified one. So where is all the excess?

If the price of say automobiles rises, yet most of the autos are purchased from Japan, then there’s your answer. Sure, some jobs were provided in America, but the excess (also known as profit) has left the country.

If the price of health insurance has risen, yet most of the insurance is purchased from domestic providers, then where is all the excess? The answer is in a broken governmental system. The government (federal and state) spends nearly twice as much on health care as does the private sector. The government gets its revenue by taxing those who are viable and paying for the health services of those who are not. The government pays less for services than does the private sector which in turn, means prices will rise for everyone to compensate for the shortfall created by government providers. Thus, prices rise, but incomes do not.

A major reason why incomes are not rising is because the cost of income taxes, social security taxes, and medicare taxes are set to rise every year. It’s not that the rates have necessarily changed, but that the income ceilings have. So you work hard to make more than the social security cap, but by the time you reach that goal, the government has raised the bar (or removed it completely). This is not a progressive tax system, it’s a progressive annual tax increase. It’s a system designed to keep our economy in chains.

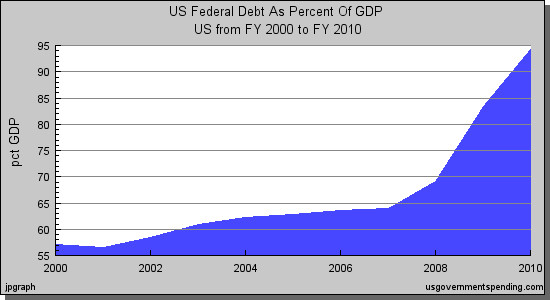

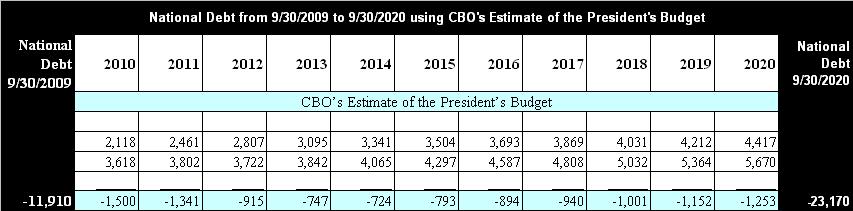

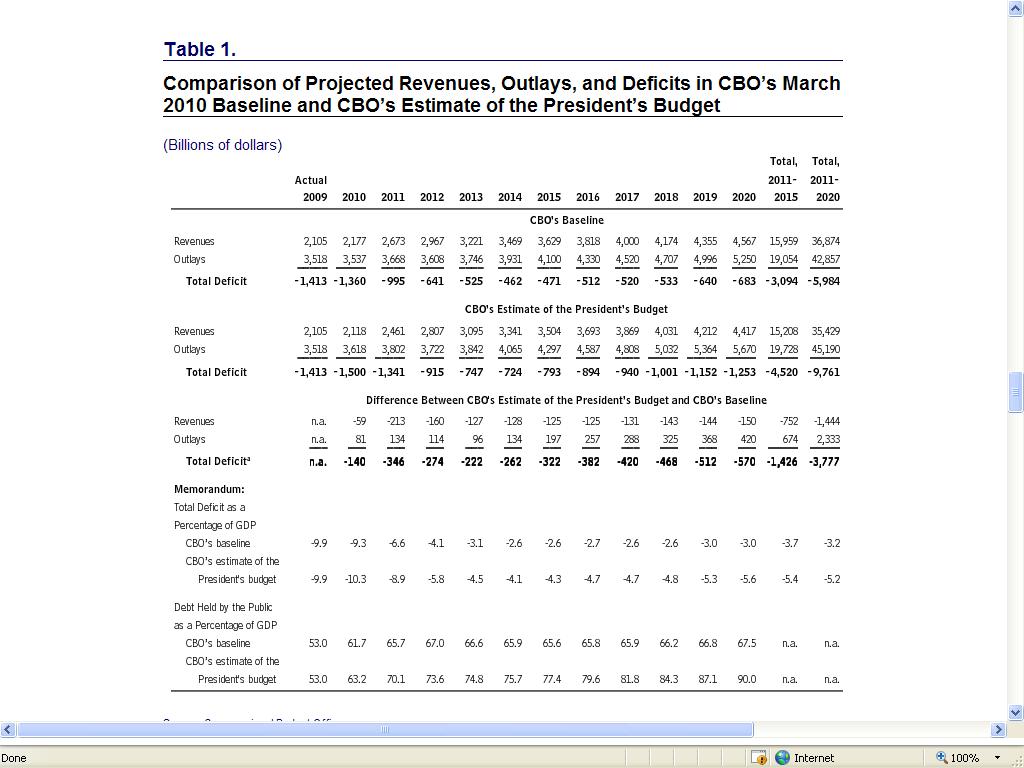

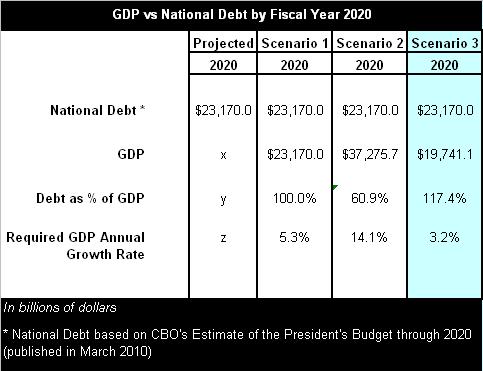

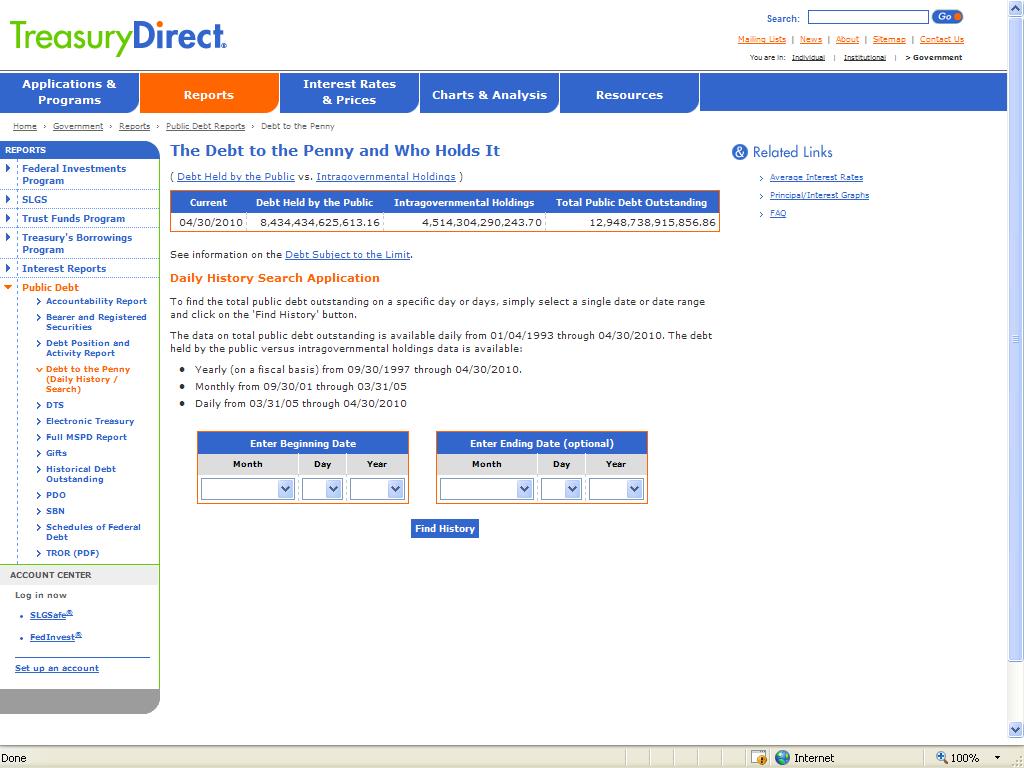

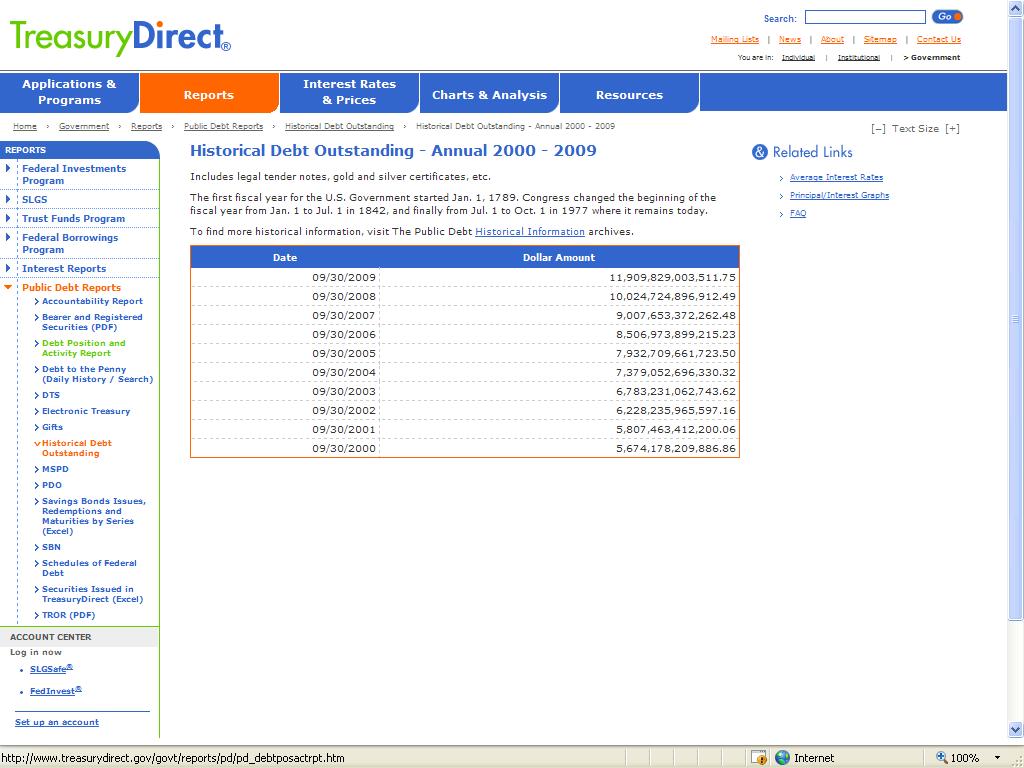

So where is all the excess? One need only look at our national debt. If there were excess, the United States Federal government would not be $13 trillion in debt. So there is no excess.

The problem lies not in price controls but rather in wealth creation. Wealth is not created through price controls. In fact, wealth is restrained by controlling prices. If prices did not rise, then neither would wealth. Yet, when wealth is not rising along with prices there is a breach.

If every American either worked for the government, or received government services, how would the government be able to continue as a going concern? The answer is that it would not. So then part of the solution, which is ingrained in your soul, is that bigger government is not the answer. On the other hand, if everyone worked in the private sector, and if everyone were able to sustain themselves, what would be the role of government? Most likely the role that was intended by our founders. So once again we can conclude that government is not the solution to our problems, government is the problem.

Message to uncle Sam, “get out of my way, and get off my back.”

End of rant….

References:

http://www.ers.usda.gov/Data/macroeconomics/Data/HistoricalRealPerCapitaIncomeValues.xls

http://stats.bls.gov/cpi/

http://www.cms.hhs.gov/NationalHealthExpendData/downloads/tables.pdf

http://www.bea.gov/national/txt/dpga.txt

Other Links and Solutions:

http://citizenownership.blogspot.com/2010/02/every-citizen-owner.html

http://citizenownership.blogspot.com/2010/02/expanded-capital-ownership-now.html

http://www.aipnews.com/talk/forums/thread-view.asp?tid=12453&posts=3#M33855

http://www.freerepublic.com/focus/f-bloggers/2460284/posts

{kind=link}