“If it sounds too good to be true, it usually is.” ~ Better Business Bureau

– By: Larry Walker, Jr. –

According to the U.S. Department of Health and Human Services (HHS), there are 7.2 million uninsured Americans ages 18 to 34 years, living in single-person households in 34 states. And, of that total, 2.9 million are eligible to buy health insurance on either federal or state partnership insurance marketplaces. And among those 2.9 million, 1.3 million, or 46%, could pay less than $50 a month for a “Bronze Plan”.

Hmmm. That sounds, well, too good to be true. Let’s see, 1.3 million times $50 equals $65 million per month, or $780 million per year. Sounds like a good deal… for insurers that is, since the balance of the monthly premium, perhaps another $50 or more, will be subsidized by taxpayers, and the risk of actually paying out any benefits, after high deductibles, co-payments and co-insurance levels are met, is next to nothing. What’s a Bronze Plan anyway, a worthless policy that covers nothing?

Generally speaking, the Bronze Plan is intended to have the lowest premium of the 4 new categories of plans (Bronze, Silver, Gold, and Platinum) but charge the highest out-of-pocket costs for healthcare services. For people without employer sponsored insurance, the Bronze plan is the minimum health insurance plan which satisfies the Affordable Care Act’s health insurance mandate.

What HHS doesn’t tell you is that Bronze Plans are designed so that policy owners wind up paying 40% or more of covered healthcare expenses in the form of out-of-pocket fees, and that’s over and above the cost of the plan’s monthly premium. Although out-of-pocket expenses for individuals are expected to be capped at $6,350, keep in mind that this amount is reset each calendar year.

Out-of-pocket expenses include fees like deductibles, copayments, and coinsurance. Different plans will approach the 40% or more that policy owner’s will pay in various ways, so it is important to research the financial details of a specific plan before deciding which one to purchase. For example, a person who has frequent medical expenses may want a Bronze Plan with a lower deductible, because they will be required to pay at least that much of their annual health care expenses – in full.

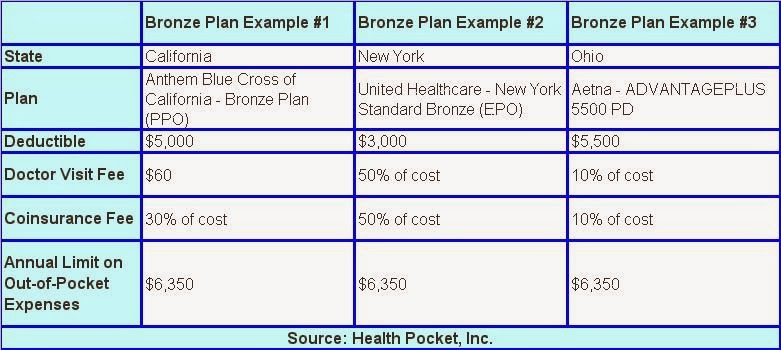

Look over the following examples of Bronze Plans, and then we’ll define the terms and discuss Example #2 in more detail.

Deductible – A deductible is the amount you pay for health care services before your health insurance begins to pay.

Coinsurance – Coinsurance is your share of the costs of a health care service. It’s usually figured as a percentage of the total charge for the service. You pay coinsurance after reaching your annual deductible.

Co-pay – A co-payment, or doctor’s visit fee, is a fixed amount you pay for a health care service, usually when you receive the service. The amount can vary by the type of service. You may also have a co-payment when you get a prescription filled.

Example #2: Okay, so let’s say the New York Bronze Plan (shown above) costs a young person $50 per month. What will he or she receive in return for this premium?

Well, since the annual deductible is $3,000, that means the insurance company won’t pay out a solitary dime, until after the insured pays the first $3,000 in annual health care costs. Then, once this $3,000 annual deductible has been met, the policy only covers 50% of the cost of doctor’s visits (co-pay), and 50% of the cost of all other medical services (co-insurance). It’s not until the insured reaches the annual out-of-pocket limit of $6,350 that the policy kicks in and pays all remaining expenses in full.

I hate to break it to you, but this alleged, under $50 per month, health insurance policy will actually wind up costing the poor sucker who buys it around $3,600 per year ($3,000 deductible + $600 premiums), or $300 per month, before it pays out a single dime in benefits. It will cost even more for plans with higher deductibles, and may wind up costing as much as $6,950 per year ($6,350 annual limit on out-of-pocket expenses + $600 annual premiums), or $580 per month, if ever actually utilized for a substantial amount of qualifying health care expenses.

Then there’s the question of which expenses such a plan actually covers, if any, once its benefits do kick in. Who in the hell knows the answer to that? Since the government’s official website is lacking in detail, even when it’s working, apparently you have to buy it first, in order to find out. Yeah, just call the toll-free number and blindly sign up. I guess it’s better than nothing, although not by much in my opinion. On this earth you get what you pay for, but the cost of nothing is generally free.

The bottom line: Don’t expect much from a health insurance plan costing less than $50 per month. If it sounds too good to be true, it usually is.

References:

How do deductibles, coinsurance and copays work?

Insurance for the young could be less than $50 a month

Bronze Plan – Affordable Care Act (Obamacare)

Related: