To: Obama and other Quasi-Socialist Progressive Fundamentalist Racism Chasers

In response to various comments regarding my last blog post: Obama on Jobs: Worst Track Record in History.

By: Larry Walker, Jr.

Actually the full quote as attributed to Economist, Thomas Sowell was: “Hope is not reality, and reality is not optional.”

Of all the jobs created, and recovered before progressives co-opted the Democrat party, how many were created by the lie that it is up to the Government to borrow money and use it to provide economic stimulus? The answer is none. The old liberal policy used to be called tax and spend (i.e. get the money first and then spend it). The tried and true conservative policy is to cut taxes and let the people spend their own money (i.e. let the free market dictate). The progressive slant has regressed into a new policy called, borrow and spend (i.e. borrow money by the trillion, spend it first, and then tax the hell out of anyone who survives).

We know that the first two methods worked to some degree, although we often disagreed on which was better. All we have to do is go back in history to measure their results. The goal has always been to grow our economy in line with the population, with limited inflation and full employment. But under this new borrow and spend philosophy, all we have is the hope that, if you are ever able to get your head above water, you will be taxed back into oblivion to pay for all the money spent to get you there. In the meantime you just hope that the $250 or $400 per year government handout is enough to get you by.

The hope that an unproven policy will be able to produce the same result as proven methods is not only uncertain, but in this matter impossible. Uncertainty is optional, but reality is not.

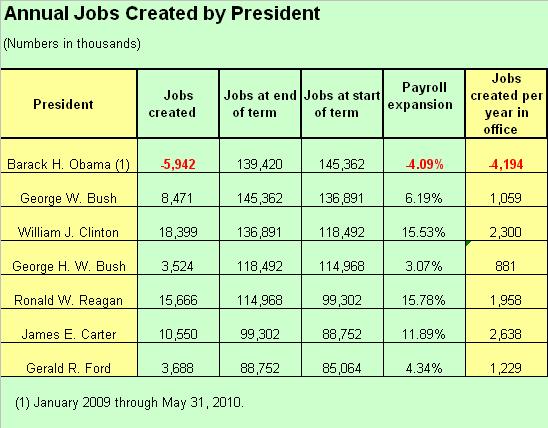

Joe Biden recently stated, “We will never be able to recover the eight million jobs that were lost.” Why would he say that? Because there is no way that it can be done under progressive ideology. It doesn’t take a rocket scientist to figure that out.

Under progressive ideology, the economy is something that will continue to function efficiently no matter which policies are crammed down its throat: stimulus, health care, energy policy, financial reform, etc… All of which may be noble goals in a fictitious world, but neither has anything to do with economic growth, nor job creation. True, each may create a few (net) jobs in the next 20 to 40 years, but there may not be any need by that time. In the end, you may be able to force all of these wonderful policies upon the peons, but by then no one will care because the great economy that once existed will be no more.

We need an economy that works for us today, not 20 years from now.

In reality, mandatory health insurance won’t do much good if there are no doctors or hospitals to visit. And where will one go to purchase it when all the insurance companies are gone? Renewable energy and carbon taxes won’t do much for the masses then living in cardboard boxes. Financial reform will be for naught if no one has any money left to save or invest. You can’t have it both ways. Either you put jobs and the economy first, or you fail on all counts.

Hoping that an unproven set of policies will work is not reality. We gave it a shot by spending well over $1 trillion, and it didn’t work. The national debt is now almost 100% of GDP and there is nothing to show for it. So what do you want to do? Do you want to keep on borrowing and stimulating until there’s nothing left? Or should we perhaps pause and consider making a u-turn? I say we heed the warning and make a u-turn before it’s too late.

We know what works, all we have to do is look back in our history at the policies that made America great.

“Reality is not optional.”

___________________________

My previous blog post may also be found at the following sites:

http://www.bookerrising.net/2010/06/larry-walker-jr-commentary-obama-on.html and,

http://aipnews.com/talk/forums/thread-view.asp?tid=15308&posts=1#M40159