Private Equity vs. Government Redistribution

– By: Larry Walker, Jr. –

“A farmer went out to sow his seed. As he was scattering the seed, some fell along the path, and the birds came and ate it up. Some fell on rocky places, where it did not have much soil. It sprang up quickly, because the soil was shallow. But when the sun came up, the plants were scorched, and they withered because they had no root. Other seed fell among thorns, which grew up and choked the plants. Still other seed fell on good soil, where it produced a crop—a hundred, sixty or thirty times what was sown. He who has ears, let him hear.” ~ Matthew 13:3-9

For many, the American Dream consists of the hope of freeloading off of the good fortune of others for their entire lives. Yet for some, the dream is comprised of one day saving enough capital to invest in a business of their own. And for a few, the dream is to one day save enough to invest through a private equity group. For those aspiring towards business ownership, sometimes a little help is needed, and that help, in many instances comes though private equity firms.

So why would anyone dream of investing in a private equity firm? Well one big reason is that under current law, around 58% of the profits realized by private equity firms are taxed as long-term capital gains rather than as ordinary income. Long-term capital gains are currently taxed at the maximum rate of 15%, while ordinary income is taxed as high as 35%. The lower tax rate on long-term capital gains helps to compensate for the opportunity cost of investing for the long haul, and also enables a greater portion of the profits to be reinvested into the next venture, which can ultimately lead to the accumulation of a great deal of wealth.

Another reason many dream of investing in private equity groups is because they feel a calling to help fellow Americans reach their dreams. Unlike bloated, deficit-financed, short-sighted, big government wealth redistribution schemes, private equity is good for America. However, if the carried interest (the long-term capital gains earned through investing in private equity) were to suddenly be taxed at the same rates as ordinary income, then there would no longer be an incentive to invest in long-term private business endeavors.

Private equity firms fund and co-manage thousands of private businesses in the United States, employing millions of American workers, and these businesses are dependent upon stable long-term investments. If big government takes away the incentive to save and invest in long-term endeavors, then there will be no long-term investment. It simply won’t be worth the risk. And without long-term private equity investment, thousands of businesses, millions of jobs and the American Dream will be choked out of existence.

Carried Interest vs. Ordinary Income

Ordinary income is mostly comprised of net business income, fixed compensation, interest, dividends, rents, royalties, and short-term (less than a year) capital gains. Unlike ordinary income, there is greater risk involved with long-term (more than a year) capital investments. Private equity firms typically make investments over a 3 to 7 year term. The risk of tying up capital savings for many years is that the investment might be lost entirely, or may not return any profit at all. So is carried interest the same as ordinary income? Centuries of sound and settled tax policies say no. But Barack Obama, a novice, with no business experience, and a track record of failed economic policies; and Warren Buffett, a retiring billionaire, who has profited from lower taxes on carried interest during his lifetime, say yes. So who’s right, centuries of proven economic science, or 32 months of butt kissing and B.S.?

The Obama-Buffett Rule presumes that carried interest is the same as ordinary income and should be taxed at ordinary income tax rates of up to 35%, instead of at capital gains rates of up to 15%. The contention that the profits earned through long-term capital investment, which involves placing previously taxed income at risk through investing in risky business ventures, which employ hundreds of thousands of American workers, and which help drive the American economy, should be taxed at the same rate as fixed compensation, such as wages earned from labor, is quite a leap. The problem with Obama’s latest Socialist twist is that unlike fixed compensation, which is properly taxed as ordinary income, carried interest, garnered through private equity investments, only rewards general partners if, at the end of the term, the fund actually results in a net gain.

To break this down further, you have on the one hand wage earners, who work 40 hours per week, get paid weekly (or semi-monthly), consume most of their pay, and have taxes withheld from each paycheck. And on the other hand, you have private equity partners who work on a project for 3 to 7 years, expending capital and sweat equity, aiding in the employment of thousands of tax paying workers, helping make tax paying businesses profitable, and ultimately hoping to, at the end of the term, regain their investment along with a handsome profit. So is carried interest the same as ordinary income? Is all income created equal? Is Capitalism the same as Socialism? Do words still have meaning?

Private Equity in Action

Within the State of Georgia there are approximately 30 private equity firms, which have invested an estimated $26 billion in Georgia-based companies, which back approximately 340 private companies, which employ more than 175,000 U.S. workers. If more capital is diverted away from private equity investments, through errant tax policies, and instead invested in tax-free securities or some other jurisdiction, then where will the capital to fund these Georgia businesses come from? It’s not likely to come from banks, which are currently paying investors taxable interest of between .01% and 1.0% on savings. And it’s not likely to come from the federal government which is currently $14.7 trillion in debt. Thus, when private equity capital is finally taxed out of existence, there will be no capital, and most of these 340 companies will cease to exist, along with 175,000 jobs.

In the State of Illinois there are approximately 137 private equity firms, which have invested an estimated $72.9 billion in Illinois companies, which back approximately 450 private companies, which employ more than 350,000 workers in the U.S. The State Employees’ Retirement System of Illinois had nearly $525 million invested in private equity as of June 30, 2008, about 5 percent of the System’s total pension fund portfolio of more than $11.4 billion. And as of June 30, 2009, the Illinois’ Teachers Retirement System had $2.34 billion invested in private equity, about 8.2 percent of TRS’ total portfolio of nearly $29 billion. Are the billions of dollars that Illinois pension funds invest in private equity firms any more or less important than any other American citizen’s savings? I think not. If the government takes away the incentive of private equity partners, then where will this capital go? If you say, “To the Banks”, again you err. If you say, “Directly into businesses”, then who will oversee and manage these investments, the government? Yeah, right, just like Solyndra.

It’s Math!

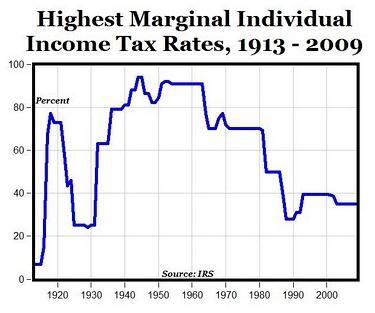

And then there’s this hogwash about wealthy people paying lower tax rates than middle income earners. Does anyone really believe this? All you have to do is glance over at one of our “progressive” tax rate schedules, to know that’s not the case. Since our tax rate structure is “progressive”, the rates increase along with income. One’s combined tax rate is never the same as their bracket rate. In other words, you may be in a 25% bracket, but that doesn’t mean you’ll fork over 25% of your taxable income. As you can see below, married couples with ‘ordinary taxable income’ of $25,000 pay a tax of 11.6%, those with $50,000 pay 13.3%, and those with $100,000 pay 17.2%; while married couples with ‘ordinary taxable income’ of $250,000 pay a tax of 24.0%, those with $1,000,000 pay 32.0%, and those with $10,000,000 pay 34.7%.

In terms of dollar amounts, on the low-end, 11.6% of $25,000 translates into $2,900, while on the high-end, 34.7% of $10 million works out to around $3.5 million. So is paying $2,900 in taxes greater than or equal to paying $3.5 million? It’s math! One must also consider that five times out of ten, that $2,900 liability gets magically turned into a tax refund of up to $8,000, as nearly half of all American workers are either not liable for any income tax whatsoever, or fall into the negative category. So perhaps the words “fair share” could be more appropriately expressed as “unfair and not-shared”.

Although it may seem fair for Obama and Buffett to compare a private equity partner with $10,000,000 of carried interest, to a married couple with taxable wages of $100,000, it’s really not. It’s like comparing oranges to apples. Although the wage earning couple will pay federal taxes of 17.2% versus the carried interest earners 15.0%, in the end, the couple will have paid a total of $17,250 in taxes, versus $1,500,000 for the private equity partner. So is $17,250 greater than $1,500,000? “It’s math!”

The real difference is that a private equity partner may then turn around and reinvest most or all of the remaining $8,500,000 into the same company that the married couple works for, thus enabling them to continue their very employment. In terms of economics, the multiplier effect on private equity investment generates many times the tax revenue paid by the partner himself. Just add up the taxes collected on all the additional wages, salaries and business profits he helps to generate. But if that capital be muzzled, the result will be less free-enterprise and even higher levels of unemployment. Thus, while earning a salary is productive, it’s nowhere near as productive as carried interest. Perhaps there’s a reason why some of our tax policies are the way they are! “It’s math!”

If Obama and Buffett really wanted to compare apples to apples, then they would be comparing a married couple with carried interest income of $10,000,000, to a couple with long-term capital gains income of $10,000,000. Each will pay $1,500,000 in taxes. So is fairness still an issue? The truth is that no American is prevented from saving his or her own money and investing in activities generating similar capital gains. Anyone can do it, and will reap an equal reward — a maximum 15% long-term capital gains tax. But if the government ever takes away this incentive, or begins to discriminate against certain forms of long-term gains, then you can kiss the American Dream goodbye.

Government Subsidies vs. Private Equity

If the government steps in and confiscates a larger chunk of the profits earned by private equity firms, then there will be that much less capital to reinvest in new acquisitions. And what will the government do to make up the shortfall? Will the government invest in and manage new enterprises? Perhaps, the federal government will subsidize more companies like Solyndra, but then who gets the ‘return on subsidy’ (ROS), if and when the government is successful? Will every taxpayer get an equal slice of the pie? That’s highly doubtful. More than likely, the money will simply be absorbed into the federal government’s irresponsible $1.3 trillion per year budget deficits, or into its $14.7 trillion national debt, or used to pay unemployment compensation, or to dole out more food stamps, neither of which will create new jobs. In other words, the money will be pilfered and consumed rather than invested in viable job creating enterprises. And we all know that America needs more jobs, not more debt, unemployment compensation and food stamps.

Private equity investors fund American businesses which employ millions of American workers. By investing in non-public companies they typically hold their investments with the intent of realizing a return within 3 to 7 years. Shouldn’t there be some reward for committing previously taxed income for 3 to 7 years, in order to help businesses grow, and to enable employment for millions of workers, with no guarantee of a profit let alone return of the original investment? I say, yes. Obama and Buffett say, no. Where they err in their quest for “fairness” is in that 42% of the profits earned by private equity investors are already taxed at ordinary tax rates, while just 58% represents carried interest. They also fail to realize that such profits are typically reinvested back into the cash account to fund the next acquisition. You would think that at least Buffett would understand this concept, since most of his earnings have been likewise reinvested.

Hell No!

With Obama’s brand of math, one would surmise that if the government could just confiscate the $1.4 trillion in annual private savings, and use it to pay the $1.4 trillion of annual government deficits this would somehow bring about “balance”. But all it would really bring about is a permanent state of depression, mass government dependency, and even greater deficits once the government runs out of other people’s money. And considering that the best the federal government could possibly do, by confiscating additional tax revenue, is to immediately absorb it into its irresponsibly amassed $14.7 trillion in accumulated deficits, over $4 trillion of which was squandered by Obama himself, the answer to the request for more revenue is still, “Hell No”. Cut spending, stop squandering the tax dollars we’re already paying, and stop regurgitating the same old lies over and over again.

Although the federal government does employ a couple of million workers, about 59% of the money used to pay them is already confiscated from taxpayers, while the other 41% is merely borrowed from the Federal Reserve Bank and from countries like China. Every dime taken away from private investors and spent by the government is a dime taken away from private businesses and private sector workers. Once the point of no return was breached, back in 2010, there was no longer enough personal income to cover the amount of federal debt, on a per capita basis, and if this is not corrected soon, it will lead to the death of the American Dream. If there is already not enough income to pay the government’s debt, then why is Obama begging for higher taxes? When there is nothing left but government, then what? Will the government pay everyone a subsidy of say $50,000, and then proceed to levy a 100% tax on everyone in order to fund itself into infinity? Isn’t this exactly where Obama’s plan leads?

The failure of Obamanomics can be summed up in a few short phrases: If it produces jobs, tax it. If it keeps producing jobs, regulate it. And when it stops producing jobs, subsidize it. Thus Obama’s plan for deficit reduction, like his Jobs Act, is just another gimmick leading to economic reduction, job destruction, government dependence, poverty and the end of the American Dream. Obama gave it his best, but his best just wasn’t good enough for America. Hey Obama, “Hell no, and good riddance.”

*** BTW – Raising the tax rate on carried interest from 15% to 35% would result in a 133.33% tax hike, or to 39.6% would equal a 164.0% hike, just in case anyone is still considering this madness. ***

“There is a limit to the taxing power of a State beyond which increased rates produce decreased revenue. If that be exceeded intangible securities and other personal property become driven out of its jurisdiction, industry cannot meet its less burdened competitors, and no capital will be found for enlarging old or starting new enterprises. Such a condition means first stagnation, then decay and dissolution. There is before us a danger that our resources may be taxed out of existence and our prosperity destroyed.” ~Calvin Coolidge (Address to the General Court beginning the 2nd year as Governor of Massachusetts January 8, 1920)

References:

Private Equity Info

Private Equity Growth Capital Council

Related:

The Problems with Raising Taxes on Carried Interest, Part II