Paying Your Fair Share

:: By: Larry Walker II ::

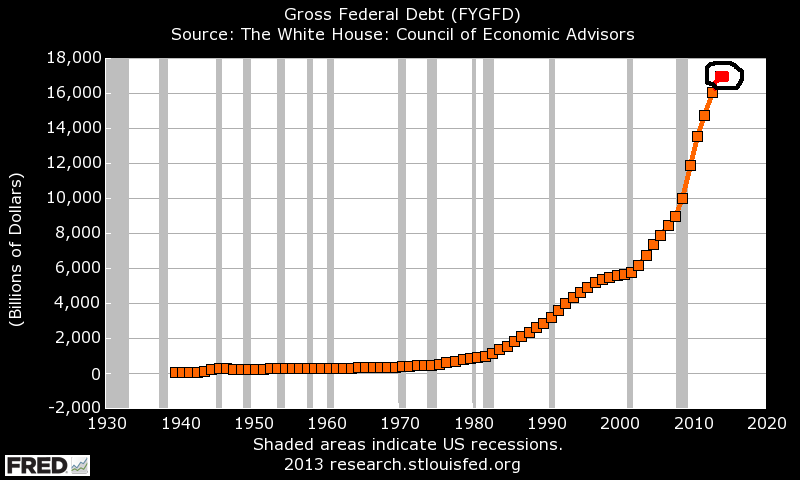

In Tax Simplification, Part II, I expounded on a 2010 Annual Report to Congress, in which National Taxpayer Advocate Nina E. Olson focused on the need for tax reform as the No. 1 priority in tax administration. In particular, she focused on the problem of delivering social benefits through the tax system, which complicates the mission of the Internal Revenue Service (IRS), resulting in a dual mission of welfare administration as well as revenue collection. But instead of taking heed, the federal government doubled down, adding a new health care excise tax and health insurance premium tax credit to the IRS’s burden.

Telephone hold times with the IRS can sometimes run as long as four to seven hours these days, and if you don’t believe me try calling yourself. A taxpayer facing a federal tax lien, levy or wage garnishment doesn’t have a choice. He or she must call immediately in order to prevent an adverse action, but unless they have a day to spare and a very powerful battery, may wind up on the phone for several days just trying to get someone on the line. The federal government has taken an agency best suited for revenue collection, and turned it into a socialist style welfare office, long lines and all.

In Part 2, I affirmed that the shared responsibility payment isn’t a fee, because nothing is received in return. Nor is it a penalty, because failure to purchase health insurance doesn’t constitute a crime. The individual shared responsibility provision imposes an excise tax on a tiny minority of U.S. residents who don’t have government-mandated health insurance or qualify for one of several exemptions. Although Internal Revenue Code – Section 5000A refers to it as a penalty, in general, if it involves filling out a federal income tax form (i.e. Form 8965), and is assessed on and payable with your personal income tax return, it’s a tax.

Opting Out

Many U.S. residents opted out of government mandated health insurance last year. Most simply couldn’t handle the government dictated concoction of monthly premiums and annual deductibles. For these, the Affordable Care Act’s punitive excise tax only makes matters worse. To those affected by this odious tax, it represents a discriminatory confiscation of wealth they are least likely to possess.

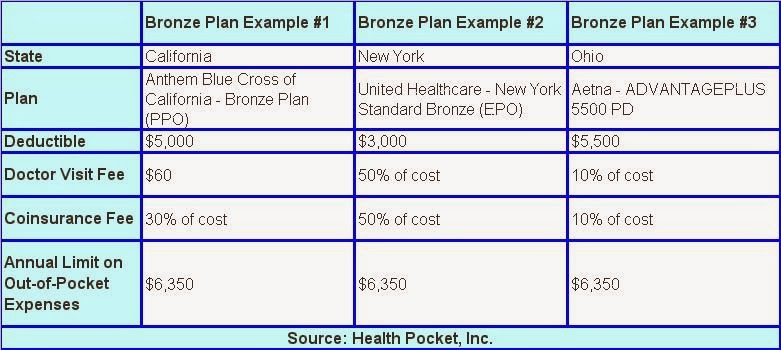

For example, the lowest cost Bronze Plan in the state of Georgia currently costs a married couple in their late 40’s to early 50’s (without children and with annual income of around $80,000) a monthly premium of around $622. Conjoined with an annual deductible of $12,600, their insurance policy won’t cover a dime of medical expenses until they have exhausted slightly over a quarter of their annual income ($20,064 / $80,000).

If the couple reasons that they may be able to afford the first $7,464 in medical bills, but would be screwed if they had to pay an additional $12,600, they would be better off not wasting their money on insurance premiums. Once having come to this conclusion, in steps the government to impose the execrated tax. The couple is then forced to hand over 1% of their income (above the filing threshold) in 2014, 2% in 2015, 2.5% in 2016, and more thereafter.

In this example, the government-inflicted excise tax is meant to encourage, or if you will, coerce the couple into purchasing a service they deemed impractical from the get go. But will it? Since the problem boils down to its exorbitant overall cost, how does a government imposed tax of $597, $1,194 or $1,493 help this couple? Newsflash: It doesn’t. Taking money away from one middle class taxpayer and handing it to another serves no meaningful purpose.

What is the purpose?

The premise behind the Affordable Care Act (ACA) was originally as follows: Too many Americans are being denied access to medical care. Health care is a fundamental right for every American. Therefore, every American should have universal access to health care. Anything less is immoral. Yet, in spite of an unprecedented level of government intervention, according to the Congressional Budget Office (CBO), roughly 30 million nonelderly U.S. residents will remain uninsured in 2016, and every year thereafter.

One critical detail, virtually forgotten in its more than 20,000 pages of regulations, is that prior to implementation of the ACA, 42 million U.S. residents were uninsured, according to an annual report from the U.S. Census Bureau. And now, after upending the entire American health care system, and throwing another monkey wrench into U.S. tax administration, come to find out that 71% of them will remain uninsured for the duration.

But at least 12 to 13 million got covered, right? Well perhaps, but not without taxpayer assistance, or what’s known in the real world as additional government debt. According to the Heritage Foundation, roughly 6 million of the newly insured were added to taxpayer-funded Medicaid programs. And according to H&R Block, the other 6.8 million purchased health insurance, but only after employing taxpayer-funded subsidies (i.e. premium tax credits).

In short, 30 million of the 42 million who were uninsured prior to the ACA will remain uninsured in 2016 and every year thereafter. And, of the 12 to 13 million newly insured, every last one received a taxpayer handout. What’s up with that? Couldn’t we have achieved the same result without maiming the tax code?

Ironically, and according to the U.S. Census Bureau, around 30 million U.S. residents, age 18 or older, never made it past the 11th grade, but that’s another story. Although not likely the same 30 million who will never have health insurance (because they get theirs for free), you can bet Progressive’s will constantly characterize them as hard-working Americans worthy of evermore governmental assistance (i.e. a higher minimum wage, free child care, free junior college, free health care, etc… etc…)

Right, so they didn’t make it past the 11th grade, but now it’s our job to hand them a free ride? Are you kidding me? These are not hard-working Americans; they are society’s losers. Close to half probably aren’t even legal. Oops! The notion of robbing the middle class, in order to dole out freebies to a bunch of flunkies is absurd. If you want something in life, work for it like the rest of us. But I digress. The affordable excise tax, being levied against the true middle class, is damnable.

Are you paying your fair share?

Now get this. Of the 30 million (or so) who will remain eternally uninsured, the majority are expected to be exempt from the new excise tax. That’s right! Despite the federal government’s ultimatum, the CBO estimates that 23 million will qualify for one or more of the following exemptions:

-

Not lawfully present. Any individual who is neither a U.S. citizen, U.S. national, nor an alien lawfully present in the U.S. If you are in the U.S. illegally, then according to the law you are exempt.

-

No filing requirement. An individual whose household income is below the minimum threshold for filing a tax return. The requirement to file a federal tax return depends on filing status, age, and types and amounts of income. If you are not required to file a return, then no other action is required.

-

Income below the federal poverty level. You were determined ineligible for Medicaid because your state didn’t expand eligibility for Medicaid under the Affordable Care Act.

-

Plans are unaffordable. You have no affordable coverage options because the minimum amount you must pay in annual premiums is more than 8% of your household income.

-

Indian tribes. Any member of a federally recognized Indian tribe. You may claim this exemption directly on your tax return through self-attestation.

-

Incarceration. Any individual in jail, prison, or a similar penal institution or correctional facility. You may claim this exemption through self-attestation when you fill out your federal tax return.

For more on exemptions, see Part 2. So in the year 2016, only around 7 million of the 30 million uninsured will have to deal with this new excise tax, in one fashion or another. The CBO estimates that among the 7 million, 3 million will either request hardship exemptions, or simply refuse to pay (i.e. take advantage of the IRS’s inability to administer and collect the tax).

All in all, the CBO believes a mere 4 million hapless Americans will be forced to fork over an estimated $4 billion in affordable care excise taxes in the year 2016. The figure climbs to an estimated $5 billion a year from 2017 to 2024. Note: The CBO neglected to offer estimates for tax years 2014 and 2015, which will likely involve higher numbers subject to the tax due to novelty of the law.

In brief, 4 million pay, while 26 million get a pass. Well, so much for the vaunted Fair Share theory! Perhaps all should be granted immunity, or at least an opportunity to purchase catastrophic health insurance policies, as I pleaded for in Part 1.

Squashing the Real Middle Class

Among the doomed 4 million (i.e. those subject to the affordable care excise tax), the CBO estimates that roughly 74% will be from what many consider to be the middle class (i.e. income exceeds 200% of federal poverty guidelines), with the remaining 26% in the low income category (i.e. income below 199% of federal poverty guidelines).Great!

So by the year 2016, out of 30 million perpetually uninsured Americans, comprising roughly 10% of the population, only 4 million, or just over 1% of the population, will be forced to pay what the Supreme Court said, “…may reasonably be characterized as a tax.” The bulk of the disheartened will represent the middle class, with a minority from the lower middle class. Wow!

Prior to the ACA, 42 million U.S. residents were uninsured. Following its implementation, 30 million, or 71%, will remain uninsured indefinitely. Of the 12 to 13 million newly insured, every single one is on the government dole, either through free Medicaid or subsidized health insurance premiums. In 2016, 4 million uninsured American citizens will be forced to hand over 2.5% of their income to the federal government in exchange for nothing, while another 26 million, in essentially the same boat, will remain uninsured but at least suffer no further humiliation. So the U.S. is finally taxing the 1%, eh?

Although the ACA focuses its excise tax on a tiny fraction of permanently uninsured Americans, at the same time it provides subsidies for people making up to four times the federal poverty line (i.e. $46,680 for a single person, $62,920 for a family of two, and $95,400 for a family of four). Can you say overpriced? As a general rule, when a product or service is subsidized it’s being sold at a premium (i.e. the insurance is overpriced). But not to worry, the ACA’s premium tax credits turn out to be a load of bull as well.

According to the Washington Examiner as many as 3.4 million of the 6.8 million who received taxpayer subsidized health insurance may owe money back to the federal government. H&R Block estimates that as many as half of the 6.8 million people who received insurance premium subsidies under the ACA benefited from subsidies that were too large. Oh, for crying out loud!

At this point, if you’re a left-winger you’re probably thinking, “Yippee, we did it!” If you’re conservative you’re likely saying, “I told you so.” And if you find yourself in the cross hairs of the affordable excise tax, you’re probably muttering words you dare not convey in public.

To be continued…

Related:

Affordable Care Excise Tax, Part I

Affordable Care Excise Tax, Part II

Affordable Care Excise Tax, Part IV

#Healthcare

Rick Perlstein said it best, “I believe politics is a team sport. That, for awful and unfortunate reasons beyond any of our control, the American system only allows, effectively, for two teams.”

Rick Perlstein said it best, “I believe politics is a team sport. That, for awful and unfortunate reasons beyond any of our control, the American system only allows, effectively, for two teams.”