“Mr. President, it is natural to man to indulge in the illusions of hope. We are apt to shut our eyes against a painful truth, and listen to the song of that siren till she transforms us into beasts. Is this the part of wise men, engaged in a great and arduous struggle for liberty? Are we disposed to be of the number of those who, having eyes, see not, and, having ears, hear not, the things which so nearly concern their temporal salvation? For my part, whatever anguish of spirit it may cost, I am willing to know the whole truth; to know the worst, and to provide for it.” ~ Patrick Henry

– By: Larry Walker, Jr. –

In following video (link), a former accountant who worked with budgets for over 40 years clearly explains the U.S. budget dilemma. After reviewing the facts contained therein, it should be evident that there are only two possible solutions for the survival of the United States: (1) raise taxes by 50% across the board or, (2) lower taxes and privatize entitlement programs.

Raising taxes leads to a smaller economy and larger government, with the need to eventually raise taxes again at some point. On the other hand, lowering taxes while privatizing entitlement programs leads to a larger economy and less government. Although the latter will cause some pain in the initial years, the affliction will be faced either way. However, privatization is the only path leading to the long-term sustainability of a free Republic.

While some would conclude that the solution involves a combination of increasing tax rates while cutting entitlement programs, I believe the two are mutually exclusive. That is to say, raising taxes reduces the size of the economy leading to the need for even more entitlements. Raising taxes also narrows the tax base leading to less government revenue. On the other hand, privatization requires lowering income tax rates to enable entitlement programs to go private. Cutting taxes also leads to a larger private economy, a broader tax base and increased government revenues. So the latter leads to greater economic independence for free citizens, and less reliance on government programs. This should be the goal for a free society.

Our freedoms may only be sustained by lowering income tax rates in conjunction with privatization of the major entitlement programs (i.e. Social Security, and Medicare). Although some painful days will occur during the initial years of conversion, in which the government must meet its past commitments while transitioning younger workers towards privatization, it is important to note that, “Every time in this century we’ve lowered the tax rates across the board, on employment, on saving, investment and risk-taking in this economy, revenues went up, not down.” Thus reducing income tax rates will actually increase, not decrease, federal revenues during the transition. Therefore, the tax cuts that I am speaking of should be across the board and immediate, as should the transition towards privatization.

There are really only two choices, (1) a larger private economy based on free-market principles and self-reliance, or (2) an ever increasing and invasive federal government with greater dependence on its ability to collect taxes from a shrinking base of those able to pay. The policies implemented today will determine America’s future. The alternatives are clear – live free, or become a ward of the State. There are no laurels to rest upon. Either you favor exercising your God-given right to freedom, or returning to slavery. The decision is yours. As for me, I choose freedom, by any means necessary.

“The day that the black man takes an uncompromising step and realizes that he’s within his rights, when his own freedom is being jeopardized, to use any means necessary to bring about his freedom or put a halt to that injustice, I don’t think he’ll be by himself.” ~ Malcolm X

Photo Credit: English Exercises

See Related:

Obsolete Government Programs, Part 1 | FICA – Apr 20, 2011

If we were not forced to pay this mandatory tax of 6.2% (12.4% for the self-employed) on earned income up to the limit of $106,800, we would be able to save a greater portion of our own money into the modern retirement…

Obsolete Government Programs, Part 2 | Medicare – Apr 21, 2011

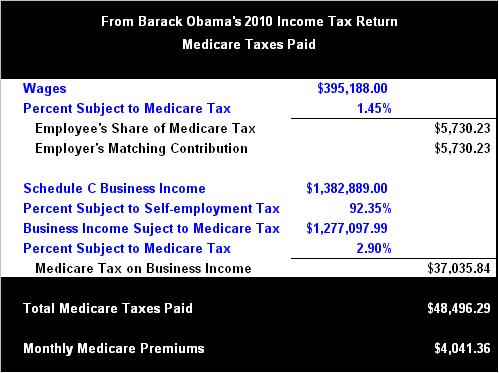

Medicare is partially financed through payroll taxes imposed by the Federal Insurance Contributions Act (FICA) and the Self-Employment Contributions Act of 1954. In the case of employees, the tax is equal to 2.9% (1.45%…

Social Security: A Breach of Trust – Jan 09, 2011

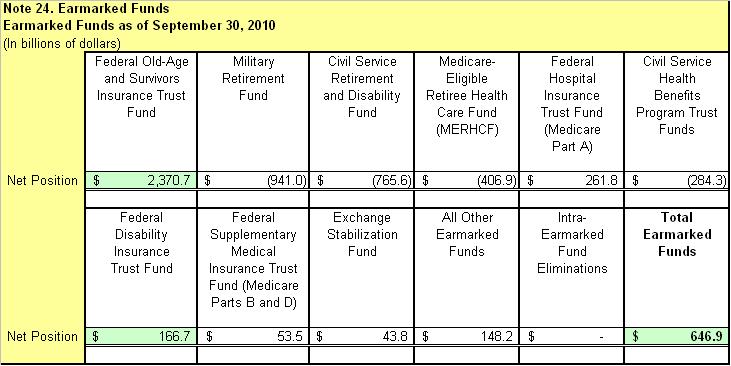

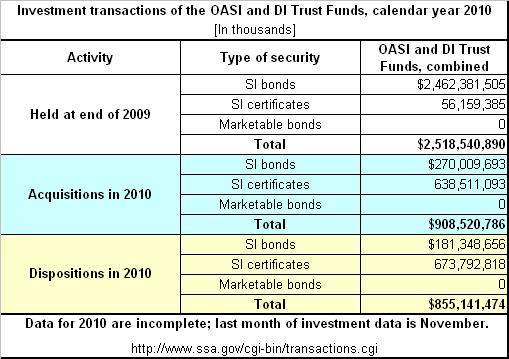

As I explained in “The Social Security Bust Fund”, the federal government has summarily confiscated and spent every dime of the $2.6 trillion surplus, which would have comprised the Social Security Trust Fund, and has…

Unequally Yoked | Social Security and the Working Class – May 07, 2011

Did you know that most state and local government employees are exempt from Social Security taxes? Millions of Americans who are covered by state or local retirement plans do not pay into the Social Security system.

The Social Security Bust Fund – Jan 03, 2011

In other words, the Treasury pays interest to the Social Security Trust Fund, but not in the form of cash, rather in the form of additional special-issue securities. (Huh?) Interest is only physically paid out when money is needed…