An Empire Built on Sand ~

~ By: Larry Walker, Jr. ~

Those of us who lived through the financial crisis of 2008 are most familiar with the drawbacks of fractional-reserve banking. It’s core theory, that wealth is created through debt, is now so ridiculously out of control, that every newborn American citizen today enters this world more than $46,000 in debt. Those naive enough to think that America’s most pressing problem started in January of 2001, or some other arbitrary date, need to look back a bit further, to 1913 to be precise. In America, taxpayers have been the suckers, while the “middle class” have been lulled into serfdom. But since we the people are no longer willing to perpetuate this fraud, the federal government, on our behalf, and at our expense, has volunteered to further prop up a broken and obsolete monetary system, yet the days of fractional-reserve banking are numbered.

What is fractional-reserve banking? – Fractional-reserve banking is a type of banking whereby a bank does not retain all of a customer’s deposits within the bank. Funds received by the bank are generally loaned out to other customers. This means that the available funds, called bank reserves, are only a fraction (reserve ratio) of the quantity of deposits at the bank. As most bank deposits are treated as money in their own right, fractional reserve banking increases the money supply, and banks are said to create money, literally out of thin air.

Fractional-reserve banking is prone to bank runs, or other systemic crisis, as anyone who has studied the American economy since 1913 is well aware. In order to mitigate this risk, the governments of most countries, usually acting through a central bank, regulate and oversee commercial banks, provide deposit insurance and act as a lender of last resort. If the banking system could only find a big enough sucker, one dumb enough to borrow say $14.4 trillion or more indefinitely, its prospects would be unlimited.

How does it work? – As an example, let’s say you work hard and are able to deposit $100,000 into Bank A. What does the bank do with your money? I mean if you wanted to withdraw it all in the following week, would it still be there? The answer is yes, and no. You see once you deposit your money, the bank immediately loans it out to someone else, likely keeping none of it in reserve, or at the most 10%. Let’s assume that Bank A is one of the mega-banks subject to the maximum bank reserve requirement of 10%. What happens is that the bank will hold $10,000 of your money either in its vault, or in a regional federal reserve bank, and will loan the other $90,000 to someone else.

Let’s say that Joe, a borrower, walks in to Bank A and applies for a $90,000 home loan on the day after you make your deposit. Bank A gladly gives Joe the $90,000 loan, at 5% interest over 30 years. When Joe closes on the loan, the $90,000 is paid to Jenn, the seller of the home. Jenn then deposits the $90,000 into her account at Bank B. Bank B keeps $9,000 of her money in reserve while lending out the other $81,000. Now let’s say that Jack comes along and secures an $81,000 business loan from Bank B on the day after Jenn makes her deposit. Now Jack deposits the $81,000 into his account with Bank C, and the cycle continues.

Bank A counts the $100,000 in your account as a liability, because it owes this amount back to you, and at the same time counts the $90,000 loan made to Joe, and the $10,000 held in reserve as assets. In effect Bank A has created a $90,000 loan asset for itself out of thin air. Fractional-reserve banks count loans as assets, and then earn their money through charging interest on this fictitious money. They also make money through repackaging loans as investments and selling them on the open market, potentially creating an even bigger fraud.

Following the money, your bank statement shows a balance of $100,000 at Bank A, Jenn’s bank statement reveals a balance of $90,000 with Bank B, and Jack has a balance of $81,000 on deposit with Bank C. The money supply has amazingly increased by $171,000 (90,000 + 81,000), through very little effort. Amazing, considering that the only real money introduced into the system was your initial $100,000 deposit. Through the system of fractional-reserve banking your original $100,000 has been magically transformed into $271,000 of liquid cash, while at the same time creating $171,000 of debt.

So what happens if you come back the following week to withdraw all of your money? Well first of all, Bank A will likely tell you that you need to give them several days notice before making such a large withdrawal, because in reality, they don’t have your money anymore. Bank A is then forced to do one of three things: borrow the money overnight from the Federal Reserve, or another member bank; sell some of its loans on the secondary market; or wait until another customer makes a $100,000 deposit – using $90,000 of that plus the $10,000 it held in reserve for you. If this sounds like a Ponzi scheme, it just might be.

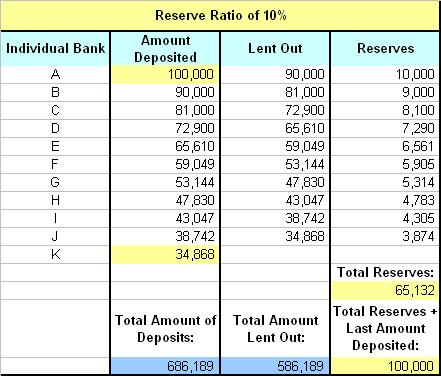

Creating Wealth through Debt – The table below displays how loans are funded and how the money supply is affected. It shows how a commercial bank creates money from an initial deposit of $100,000. In the example, the initial deposit is lent out 10 times with a fractional-reserve rate of 10% to ultimately create $686,189 of commercial bank money. Each successive bank involved in this process creates new commercial bank money (out of thin air) on a diminishing portion of the original deposit. This is because banks only lend out a portion of the initial money deposited, in order to fulfill reserve requirements and to allegedly ensure that they have enough reserves on hand to meet normal transaction demands.

The model begins when the initial $100,000 deposit of your money is made into Bank A. Bank A sets aside 10 percent of it, or $10,000, as reserves, and then loans out the remaining 90 percent, or $90,000. At this point, the money supply actually totals $190,000, not $100,000. This is because the bank has loaned out $90,000 of your money, kept $10,000 of it in reserve (which is not counted as part of the money supply), and has substituted a newly created $100,000 IOU for you that acts equivalently to and can be implicitly redeemed (i.e. you can transfer it to another account, write a check on it, demand your cash back, etc.). These claims by depositors on banks are termed demand deposits or commercial bank money and are simply recorded on a bank’s books as a liability (specifically, an IOU to the depositor). From your perspective, commercial bank money is equivalent to real money as it is impossible to tell the real money apart from the fake, until a bank run occurs (at which time everyone wants real money).

At this point in the model, Bank A now only has $10,000 of your money on its books. A loan recipient is holding $90,000 of your money, but soon spends the $90,000. The receiver of that $90,000 then deposits it into Bank B. Bank B is now in the same situation that Bank A started with, except it has a deposit of $90,000 instead of $100,000. Similar to Bank A, Bank B sets aside 10 percent of the $90,000, or $9,000, as reserves and lends out the remaining $81,000, increasing the money supply by another $81,000. As the process continues, more commercial bank money is created out of thin air. To simplify the table, different banks (A – K) are used for each deposit, but in the real world, the money a bank lends may end up in the same bank so that it then has more money to lend out.

Although no new money was physically created, through the process of fractional-reserve banking new commercial bank money is created through debt. The total amount of reserves plus the last deposit (or last loan, whichever is last) will always equal the original amount, which in this case is $100,000. As this process continues, more commercial bank money is created. The amounts in each step decrease towards a limit. This limit is the maximum amount of money that can be created with a given reserve ratio. When the reserve rate is 10%, as in the example above, the maximum amount of total deposits that can be created is $1,000,000 and the maximum increase in the money supply is $900,000 (explained below).

Fractional reserve banking allows the money supply to expand or contract. Generally the expansion or contraction is dictated by the balance between the rate of new loans being created and the rate of existing loans being repaid or defaulted on. The balance between these two rates can be influenced to some degree by actions of the Fed. The value of commercial bank money is based on the fact that it can be exchanged freely as legal tender. The actual increase in the money supply through this process may be lower, as at each step, banks may choose to hold reserves in excess of the statutory minimum, or borrowers may let some funds sit idle, or some people may choose to hold cash (such as the unbanked). There also may be delays or frictions in the lending process, or government regulations may also limit the amount of money creation by preventing banks from giving out loans even though the reserve requirements have been fulfilled.

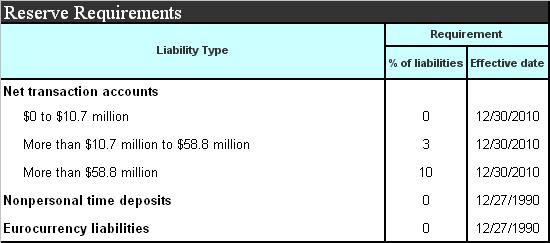

What are the Fed’s current reserve requirements? – According to the Federal Reserve, banks with less than $10.7 million on deposit are not required to reserve any amount. When deposits reach $10.7 to $58.8 million the requirement is just 3%. It’s only when deposits exceed $58.8 million that a 10% reserve requirement applies. The table below was extracted from the Federal Reserve’s website.

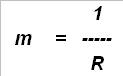

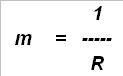

How much money can our banking system create out of thin air? – The most common mechanism used to measure the increase in the money supply is typically called the money multiplier. It calculates the maximum amount of money that an initial deposit can be expanded to with a given reserve ratio.

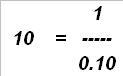

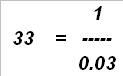

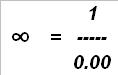

Formula – The money multiplier, m, is the inverse of the reserve requirement R:

Examples

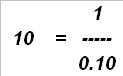

A reserve ratio of 10 percent yields a money multiplier of 10. This means that an initial deposit of $100,000 will create $1,000,000 in bank deposits.

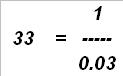

A reserve ratio of 3 percent yields a money multiplier of 33. This means that an initial deposit of $100,000 will create $3,300,000 in bank deposits.

A reserve ratio of 0 percent yields a money multiplier of ∞ (infinity). This means that an initial deposit of $100,000 will create an unlimited amount of bank deposits.

What’s the problem? – The system works fine as long as everyone plays along. The biggest problem is that it’s a system by which wealth is only created through debt. Through this system, the lender always wins; while debtors – nowadays referred to as the middle class – always lose. As long as there are willing borrowers, our economy grows. When consumers, businesses, and the federal government stop borrowing, the system shuts down. But one cannot very well borrow into infinity; after all, life itself is finite. “There is a time to borrow, and a time to repay; a time to live and a time to die.” One definitely cannot borrow while lacking the means of repayment, unless of course, it has a seeming unlimited ability to tax.

The next biggest problem is that of absurdly low bank reserve requirements. With bank reserve requirements set at 0% to 10%, what could possibly go wrong? I mean besides banks having the ability to create an infinite supply of make-believe money through debt. The modern mainstream view of reserve requirements is that they are intended to prevent banks from:

- Generating too much money by making too many loans against the narrow money deposit base;

- Having a shortage of cash when large deposits are withdrawn (although the reserve is thought to be a legal minimum, it is understood that in a crisis or bank run, reserves may be made available on a temporary basis).

Let’s face the facts. Our present monetary policy is a disaster. When too many players wish to withdraw their money to hold as cash, or too many purchases are made overseas, or an excessive amount of loan defaults occur, the house comes crashing down. When all three events occur at the same time, as actually happened in 2008, it should have spelled the end of fractional-reserve banking. But instead, our leaders are in denial. Now “wealthy” U.S. taxpayers are being called upon to bailout the federal government, while at the same time, the government seeks more borrowing power. But when all our wealth is gone, who will rescue us then? And if the entire global monetary system has likewise been built on the same sinking sand, who will rescue them?

Well, hopefully you now have a better understanding of why our present monetary system is dysfunctional, why the federal government wants you to borrow more, and why it wants to borrow more itself. We are a nation built on a Ponzi scheme; one which cannot grow without incurring further debt. But as I said before, growth through debt amounts to nothing more than spending next year’s income today. Man does not live by debt alone.

What’s the solution? – We have to put an end to fractional-reserve banking. It should be clear, to all those with understanding that we need to get off of this merry-go-round. The first step is for the Federal government to take the power of money creation away from the Federal Reserve and from commercial banks by both issuing and controlling the quantity of its own currency (rather than Federal Reserve Notes). The second step is to increase bank reserve requirements to 100%, as banks should never again be allowed to loan out more money than actually on deposit. If there was a way to end the debt-money system and to payoff the national debt within a year or two, wouldn’t you want to know? For the details on how to accomplish this, I implore you to watch Bill Still’s full video entitled, The Secret of Oz (preview).

“Therefore everyone who hears these words of mine and puts them into practice is like a wise man who built his house on the rock. The rain came down, the streams rose, and the winds blew and beat against that house; yet it did not fall, because it had its foundation on the rock. But everyone who hears these words of mine and does not put them into practice is like a foolish man who built his house on sand. The rain came down, the streams rose, and the winds blew and beat against that house, and it fell with a great crash.” ~ Matthew 7:24-27 (NIV)

References:

Fractional-Reserve Banking

Principles of Monetary Reform

Federal Reserve: Monetary Policy