* More Honest Debate *

By: Larry Walker, Jr. –

What is a Cooperative (Co-Op)? *

A Cooperative is a business organization owned and operated by a group of individuals for their mutual benefit. A cooperative may also be defined as a business owned and controlled equally by the people who use its services or who work at it.

There are many types of Co-Ops in the United States. I will attempt to address some of the most common cooperatives. If you belong to a credit union, you are already a member of a Co-Op. My electric and natural gas utility company is an EMC, another word for Co-Op. In the insurance industry, Co-Ops are called Mutual Companies, or Mutual Legal Reserves.

Credit Unions are owned by their members. When you join, you must establish a share account and maintain a minimum balance. Your share account is your capital investment in the company. You are paid ‘dividends’ on your savings and checking accounts. Dividends are your share of the Credit Union’s profits. A Credit Union offers benefits for its members such as preference on home and automobile loans.

An Electric Membership Corporation (EMC) is a service cooperative owned by those who receive its services. There are nearly 1,000 electric cooperatives in the United States. When the EMC makes a profit, those profits are shared with customers through credits to their electric bills, or lower rates.

Health Insurance Co-Ops

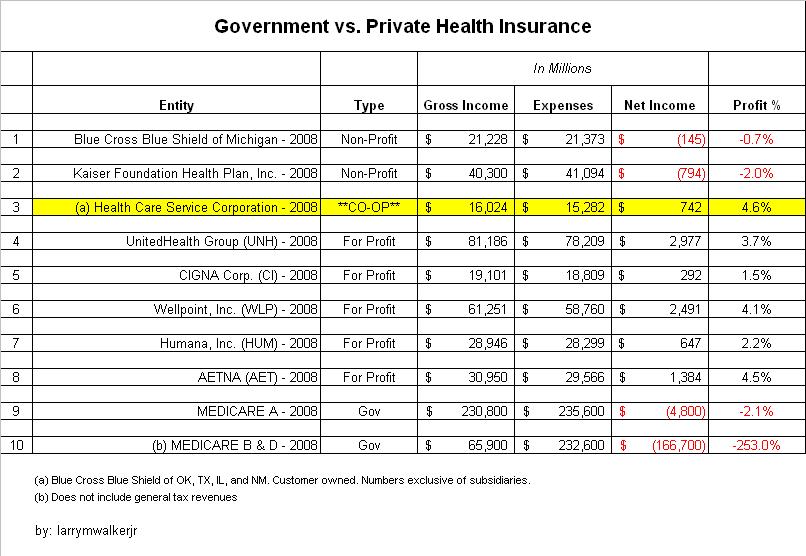

Health Care Services Corporation (HCSC) is the largest customer owned health insurer in the United States.

-

HCSC operates the Blue Cross and Blue Shield plans in Illinois, New Mexico, Oklahoma and Texas, employing 17,000 people and serving more than 12.4 million members – 38% in national employer plans, 32% in large local employer plans, 10% in small employer plans, 10% in individual plans and 10% in government plans.

-

HCSC is the fourth largest health insurance company in the United States and the largest customer-owned health insurer. In 2008, the company’s gross revenue totaled $39.9 billion (considering all subsidiaries which are not included in the chart below in accordance with GAAP).

-

HCSC is the most financially secure health insurer in the United States, with a rating of AA- (Very Strong) from Standard and Poor’s, Aa3 (Excellent) from Moody’s and A+ (Superior) from A.M. Best Co.

-

HCSC retains full or joint ownership of a number of subsidiary companies, including Fort Dearborn Life Insurance Co., Dental Network of America, MEDecision, Availity, Prime Therapeutics and RealMed.

If the HCSC model is the type of Health Insurance Co-Op being discussed in Congress, then I am a fan. Yes. Here is an idea that would have strong bi-partisan support. We can agree on Health Insurance Co-Ops. In my opinion Co-Ops are in line with the purest sense of Capitalism. On the other hand, if Congress is talking about some kind of partially Government owned, or Government controlled entity, then I am not in favor.

In fact, I would like to join HCSC, or a similar Co-Op, but unfortunately it only operates in 4 states, and none of the health insurers in my state are co-ops. Fostering increased competition by allowing insurers to operate in all states would be an improvement.

The Plan

So if America wants to convert its health insurance industry to Co-Ops, the question is how? Obviously, it would be unfair, and foolish, to force the existing insurers out of business, so how do you get them to convert?

I am a proponent of Binary Economics. Under Binary Economics, the only role of Government in private enterprise is to offer interest-free loans through its central bank. Existing publicly traded insurers will need to buy back all of their stock in order to make the conversion to mutual companies. Interest free loans from the Government will facilitate this conversion. The loans will be paid back over the long-term out of the profits of the insurers. Once the loans have been paid, the insured will be able to participate in a larger share of company profits. Profits will be shared with policy holders either in the form of dividends, or lower insurance rates.

Interest free loans are not hand-outs, or bailouts. The money gets paid back. Granting interest free loans would be a much better use of taxpayers money than the current foolishness being promoted by certain ‘linear’ thinkers (right and left). The World is not flat. In fact, most good ideas come from outside of the box.

Reforms I can believe in:

-

Conversion of the Health Insurance Industry to Co-Ops

-

Tort Reform

-

Fostering Interstate Commerce for increased competition

-

No denial for preexisting conditions

-

Tax Incentives for those paying higher premiums due to preexisting conditions

-

Tax incentives for purchasing health insurance

-

Portability of policies

Reforms I don’t believe in:

-

Making health insurance mandatory

-

Taxing employers who don’t offer insurance

-

Expanding Government-Run health care

-

Excessive Government Regulation

-

Triggers

click images to enlarge

Sources:

http://www.hcsc.com/about-hcsc/overview.html

http://www.investopedia.com/terms/m/mutualcompany.asp

http://en.wikipedia.org/wiki/Co-op

http://www.waltonemc.com/mycoop/

https://blackandcenter.blog/2009/09/02/government-run-vs-private-health-insurance/