The Fiscal Responsibility Cliff

– By: Larry Walker –

When I went to work for the IRS back in 1988, the first few weeks were spent in tax law courses. I distinctly remember, at the time, that the base amounts used in determining the taxability of Social Security benefits were $25,000 for single taxpayers and $32,000 for married taxpayers filing a joint return. For some reason when the topic came up this year, during annual continuing education, with all the talk of looming fiscal responsibility (errantly referred to as a cliff), combined with having been read the riot act by several seniors over the past year, it suddenly dawned on me that the base amounts are exactly the same in tax year 2012 as they were in 1985 –– $25,000 and $32,000. What’s wrong with this picture? The same thing that’s wrong with Barack Obama’s $250,000 top tax bracket argument, a failure to adjust for inflation.

My first brush with tax law was actually through a Junior College course in 1981. I helped prepare tax returns commercially for several years thereafter while attending college. Needless to say, I left the IRS in 1994 and moved on to brighter horizons. I returned to my first love in the year 2000 and am still involved in the industry today. With that out of the way, what’s both interesting and disturbing to me is the fact that Social Security benefits were tax-free prior to 1985, but then Congress, in its wisdom, changed the law to ensure that wealthy seniors were paying their fair share, which by my logic merely amounted to forcing them to pay taxes on the taxes they had already paid.

It was in 1985 that a neat little formula was devised whereby if one-half of a taxpayers Social Security benefits plus their other income (both taxable and tax-exempt) was more than the base amount (mentioned above), then up to half of their Social Security benefits would become taxable. As a consolation, if a senior’s sole source of income was Social Security, in other words if they were living near or below the poverty line, then none of the benefits were taxable.

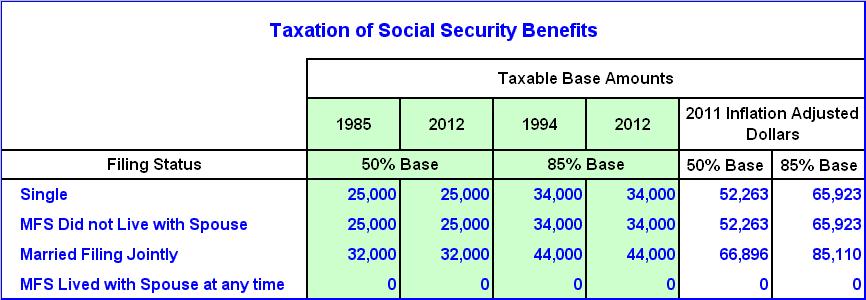

According to the formula, if you are single or married filing separate and did not live with your spouse for the entire year, the base amount is $25,000. If you are married and file a joint return, the base amount is $32,000. And if you are married filing separate but lived with your spouse at anytime during the year, the base amount is $0. To determine how much of your benefits are taxable, you add one-half of your Social Security benefits to other income received from pensions, interest, dividends, capital gains, rental income, business income, tax-exempt interest, etc…, and then subtract from this the applicable base amount. If the result is positive, then the taxable amount of your Social Security benefits is the lesser of one-half of the result, or one-half of your Social Security benefits. Got it?

The obvious dilemma is that the base amounts are exactly the same today as they were in 1985 –– $25,000 and $32,000. Something is deftly wrong with this, because when adjusted for inflation the base amounts become $52,263 and $66,896. That’s a material difference, more than double. In my opinion, if Congress would simply index all limitations, base amounts and tax brackets for inflation (the AMT comes to mind), then the U.S. income tax system would be fair, but as it stands today for many it is not.

Making matters worse, beginning in 1994 Congress decided to up the ante. Taxing 50% of Social Security just wasn’t enough for really rich old folks, so Congress added a second set of base amounts, whereby up to 85% of benefits could become taxable. To distinguish wealthier seniors from the rest, the original base amounts were raised by $9,000 for single filers and by $12,000 for joint filers. Thus, if one-half of your Social Security benefits, plus other income (both taxable and tax-exempt) was greater than $34,000 or $44,000, respectively, then up to 85% of the difference, or 85% of your Social Security benefits were taxable, whichever was less. The same amounts are in force today. There has been no inflation adjustment to the 85% base amounts since 1994.

If the 50% and 85% base amounts were rightly adjusted for inflation, then the former would rise from $25,000 and $32,000, to $52,263 and $66,896; and the latter would increase from $34,000 and $44,000, to $65,923 and $85,110 (see table below).

Now that’s more like it. It’s not all that, but it’s better than what we have today. Inflation Indexing should be an integral part of tax reform. It’s not right to screw our seniors out of money, when an automatic adjustment is granted in other areas of the tax code. We should have more respect for our elders. But even though my proposal would be an improvement, still the premise behind taxing Social Security benefits is errant.

Can you understand why so many seniors complain? Here’s what one fellow said to me recently, “What do you mean 85% of my Social Security is taxable? It wasn’t taxable at all last year. Just because I was finally able to make a little extra money this year, you mean to tell me that now I have to pay half of what I made in taxes? You’re telling me that I’m going to owe about half of what I’ve been able to save this year in taxes. I paid into the system my whole life, that money should be tax free. I might as well just stop working if I’m going to owe half of what I make in taxes, but then how am I supposed to live?”

I basically agreed with him. What he said is true. If you are self-employed and on Social Security, and make around $50,000 on the side, by the time you add in 85% of your Social Security benefits, $50,000 suddenly becomes $60,000 or more. Then when you add together the applicable self-employment taxes, federal income taxes and state taxes, the marginal tax rate quickly approaches 50%. I opined that I think anyone over 65 should be exempt from paying into Social Security while they are receiving benefits, and that the benefits should be tax free. I qualified this by adding that I don’t write the laws, I just apply them.

Congress should recall that we pay Social Security taxes in order to receive a basic subsistence in the future. The Social Security taxes we pay are a tax. Then the federal government has the nerve to turn around and tax seniors on the taxes they have already paid throughout their lives. In effect, what seniors are asked to do is pay a tax on a tax. How much sense does that make in the era of fair this and fair that? You have to admit that this is messed up. So fix it! It’s real simple.

Congress should either increase the Social Security base amounts for inflation, or go back to the pre-1985 policy making Social Security benefits non-taxable, and let the cards fall where they may. Make a choice and live with it. Anyone in Congress, or the White House who doesn’t have a clue about what’s in the current tax law, should study up, shut up, or just resign. Anyone who takes the time to examine what’s actually in the Code will come to the realization that some of this stuff is completely ridiculous. Under current law, it is entirely possible to make over $250,000, write it all off through new equipment purchases, other credits and gimmicks, and end up paying nothing in taxes. Yep, that’s right!

In my opinion, what we need to do is get rid of all of the temporary 2010 provisions including –– repeal of the Personal Exemption Phase-Out (PEP), repeal of the Itemized Deduction Limitation (Pease), 0% Capital Gains Tax, expanded Child Tax Credit, expanded Dependent Care Credit, increased Adoption Credit, increased Earned Income Credit, refundable Education Credit, Alternative Minimum Tax (AMT) patch, Bonus Depreciation, extended Section 179 Deduction, Payroll Tax Cut, and the vast array of Energy Tax Credits, and then go back to the 1986 Code and adjust all limitations, base amounts and tax brackets for inflation. In most cases, just like with Social Security benefits, the results will favor those who are the most deserving. We got by without this chaos before 2010, and we can get by without it today.

Fiscal responsibility isn’t a cliff, it’s an opportunity to correct our errant ways. Respect your elders. By the way, the notion of lowering the top income tax bracket from the current inflation adjusted amount, to the 1993 unadjusted top bracket of $250,000 is equally offensive. That’s not forward thinking. In fact, it’s so backwards it’s laughable. Think inflation!

References:

Related:

Comment on Free Republic: Don't forget….Almost every senior over 65 collecting SS is paying $100 ($1200 a year) out of that check for Medicare Part B……in addition to what they had already paid into it before age 65… And they have to buy a supplement, too.

Response: Good point. And neither is subtracted out when determining the taxability of Gross Benefits in Box 5 on the SSA-1099.

LikeLike

Pingback: Phantom Tax Credit for Elderly and Disabled | Black and Center

Pingback: Tax Fairness | Reverse Parity | Black and Center